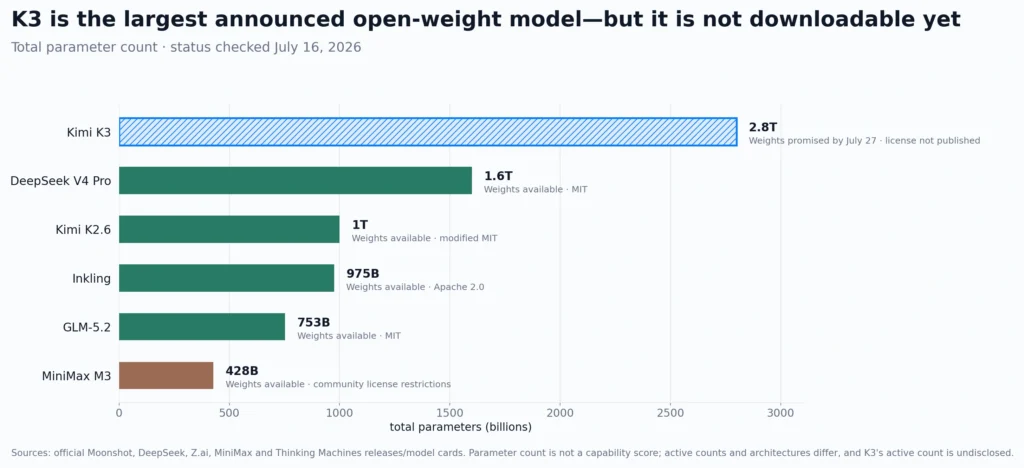

On July 16, Beijing-based Moonshot AI released Kimi K3, a 2.8-trillion-parameter model that instantly became the largest open-weight AI system ever announced — and, depending on which benchmark you squint at, one of the three or four most capable models on the planet. Within 48 hours, chip stocks had wobbled, a rival Chinese lab had lost nearly a third of its market value, and half the AI internet had declared a second DeepSeek moment.

Most of that coverage is running on autopilot. The reflexive take — cheap Chinese model crashes the party, closed labs in trouble, race to the bottom — misses the two details that actually matter. First, Kimi K3 is not cheap. It launched at flagship pricing, a deliberate break from the discount positioning that made its predecessors famous. Second, the benchmark horse race is the least interesting part of this story. The interesting part is economic: when frontier-class capability ships with downloadable weights and a permissive license, what happens to everyone building on top of AI? Does the application layer bloom, or does it get flattened? Who captures the value — and who quietly loses their moat?

This is a deep dive into those questions. We will lay out what Kimi K3 actually is, why its pricing surprised almost everyone, where it really stands against Claude Fable 5, GPT-5.6, and the rest of the frontier field, and then work through the evidence on the question that matters most: whether the proliferation of powerful open models leads to more AI applications being built, or fewer. We will weigh both cases honestly, because both have real evidence behind them — and the answer shapes strategy for every AI company, developer, and investor reading this.

What Is Kimi K3? Specs, Architecture, and the Launch Details

Kimi K3 is the third major generation of Moonshot AI’s Kimi model line, launched on July 16, 2026 — timed, not coincidentally, to land just ahead of the World Artificial Intelligence Conference in Shanghai, and in the same news cycle as Xi Jinping’s first appearance at China’s premier AI summit. The headline numbers: roughly 2.8 trillion total parameters, a 1,048,576-token context window, native visual understanding, and reasoning that runs at maximum effort by default. It is available now through the Kimi app, kimi.com, and an OpenAI-compatible API, with two consumer-facing variants — K3 Max for chat and agent work, and a Swarm Max tier built for large-scale parallel sub-agent execution.

The architecture: sparse by design

The 2.8-trillion figure deserves an immediate asterisk, because it describes capacity, not per-token compute. K3 is a mixture-of-experts model: of its 896 expert subnetworks, only 16 activate for any given token. That is the trick that makes a model this size servable at all, and it continues the design philosophy of Kimi K2.6, which packed one trillion total parameters into roughly 32 billion active ones. K3 also debuts a new attention stack — Kimi Delta Attention, a hybrid linear-attention mechanism paired with attention residuals — which is Moonshot’s answer to the brutal economics of serving a one-million-token context window. The company reports cache hit rates above 90% on coding workloads, which matters enormously for real-world cost, as we will see below.

The addition of native vision is a bigger deal than it sounds for the workloads Moonshot is chasing. K3 is positioned squarely at long-horizon coding and agentic work — navigating large repositories, iterating against logs, tests, screenshots, and runtime feedback. That positioning is backed by a real ecosystem: the Kimi Code CLI, Moonshot’s open-source answer to terminal coding agents, shipped two upgrades the same day K3 launched and now integrates with VS Code, Cursor, and Zed.

Open-weight, not quite open-source — and not until July 27

Here is the nuance most headlines flattened: as of this writing, you cannot download Kimi K3. Moonshot has committed to publishing the full weights on Hugging Face by July 27 under a Modified MIT license — the same license family used for the K2 generation, which permits commercial use and redistribution with limited conditions. Until the files actually land, K3 is an API-only model wearing an open-source press release. And “open-weight” is the precise term rather than “open-source”: training data, full training code, and methodology remain Moonshot’s. That distinction matters for reproducibility, auditability, and for anyone whose compliance team asks hard questions.

Even once the weights drop, self-hosting is not a laptop hobby. At 2.8 trillion parameters, even an aggressive ~2-bit quantization implies something on the order of 700 GB before runtime overhead — practical deployments will want 650 GB to a terabyte of accelerator memory. The realistic consumers of these weights are inference providers, large enterprises, and well-funded startups, not individual tinkerers. That shapes the economics of everything that follows.

The company behind it

Moonshot AI was founded in 2023 by researcher Yang Zhilin, is backed by Alibaba, and has ridden a remarkable arc: a $500 million Series C in January 2026 at a $4.3 billion valuation — money explicitly earmarked for K3’s training compute — followed by a $2 billion raise in May at a valuation above $20 billion. Post-launch reporting suggests the company is already in talks at a $31.5 billion valuation. Whatever else K3 is, it is proof that open-weight releases and eleven-figure valuations are no longer in tension. That fact alone should recalibrate how Western observers think about the economics of open models.

Kimi K3 Pricing: The Part Almost Everyone Got Wrong

If you absorbed the K3 story through headlines, you probably assumed it undercuts everything. It does not. Kimi K3’s API pricing is $3.00 per million input tokens and $15.00 per million output tokens, with cached input at $0.30 per million — flat across the entire one-million-token context window, with no long-context surcharge. Consumer access runs through Kimi subscription plans from $19 to $199 per month, with context length tiered by plan.

Put that in context and the strategy snaps into focus. Kimi K2.6 launched at $0.60 input and $2.50 output — meaning K3 costs five times as much on input and six times as much on output as its own predecessor. Within the Chinese open-model cohort, K3 is now the expensive option by a wide margin: DeepSeek V4 output runs around $0.87 per million tokens and Zhipu’s GLM-5.2 around $4.40, against K3’s $15. The bargain framing only survives when you look upward: K3 still undercuts Claude Opus 4.8 (about $5/$25), GPT-5.6 (about $5/$30), and sits far below Claude Fable 5, whose output pricing reaches $50 per million tokens.

| Model | Input ($/M tokens) | Output ($/M tokens) | Positioning |

|---|---|---|---|

| Kimi K3 | $3.00 ($0.30 cached) | $15.00 | Open-weight frontier flagship |

| Kimi K2.6 (launch pricing) | $0.60 | $2.50 | Prior Moonshot flagship |

| Kimi K2.7 Code | $0.95 | $4.00 | Coding workhorse |

| DeepSeek V4 | from ~$0.14 (Flash) | ~$0.87 | Open-weight value leader |

| GLM-5.2 (Zhipu) | — | ~$4.40 | Open-weight mid-tier |

| Claude Opus 4.8 | ~$5.00 | ~$25.00 | Closed frontier |

| GPT-5.6 | ~$5.00 | ~$30.00 | Closed frontier |

| Claude Fable 5 | — | ~$50.00 | Closed frontier flagship |

Reported list pricing at K3’s launch week, July 2026. Model pricing changes frequently; treat as a snapshot, not gospel.

Two wrinkles complicate the sticker price in opposite directions. Working against K3: reasoning is always on at maximum effort, with no dial to turn it down, and long agentic loops can inflate output token counts dramatically — output is where K3 charges most. Working in its favor: that $0.30 cached-input rate combined with claimed 90%-plus cache hits on coding workloads can cut effective input costs to a fraction of the sticker, if you structure prompts around a stable prefix. Real-world K3 economics will vary more between well-engineered and naive integrations than between K3 and its listed rivals.

So why price a supposedly open model like a closed flagship? Because Moonshot can — for a window. Until July 27, the only place to run K3 is Moonshot’s own infrastructure, and the company is monetizing exclusivity while it lasts. The moment the weights land on Hugging Face, the dynamic inverts: third-party inference providers will race to serve it, quantized builds will appear within days, and price competition on identical weights will begin grinding the effective cost down. That is exactly the arc Kimi K2 and DeepSeek followed. Moonshot captures flagship margins during the exclusivity window and buys developer mindshare with the open release afterward. It is a genuinely clever sequencing — and it means the number to watch is not today’s $3/$15, but what the serving market charges for K3 in September.

Kimi K3 Benchmarks: Where It Actually Stands

Moonshot’s own framing was unusually candid for a launch: the company said K3’s overall performance still trails Anthropic’s Claude Fable 5 and OpenAI’s GPT-5.6 Sol, while claiming frontier-level results overall and wins over earlier closed models. On coding and agentic benchmarks specifically, Moonshot says K3 performed competitively with Fable 5 and substantially outperformed Claude Opus 4.8 and GPT-5.5. VentureBeat’s review of the launch materials found K3 placing top-three across six coding benchmarks, leading the field on SWE Marathon and Program Bench and trailing GPT-5.6 Sol by half a point on Terminal Bench 2.1 — with every model tested at maximum thinking effort.

Independent signals so far point the same direction, with scatter. Artificial Analysis slots K3 at fourth of 189 models on its Intelligence Index, a single point ahead of Claude Opus 4.8. One arena-style leaderboard has even ranked K3 first outright — an outlier worth noting and discounting in the same breath. The honest synthesis: K3 is the strongest open-weight model ever released, sits just below the two closed frontier leaders on aggregate capability, and is genuinely elite at the coding-agent workloads it was built for. Bank of America analysts drew the sharper conclusion in a client note: despite constrained access to top-end chips, Moonshot demonstrated that training and architecture innovation can substitute for raw compute. That, more than any single score, is what rattled markets.

The standard caveats apply with extra force here. Most of these numbers are vendor-reported, the weights are not yet public for independent replication, and always-on maximum reasoning makes cross-model comparisons sensitive to configuration. The verification window opens July 27. Until then, treat every K3 bar chart — including Moonshot’s — as a claim, not a finding. For how the full frontier field stacks up beyond K3, see our frontier model comparison and the GPT-5.6 family breakdown.

The Market Reaction: A Second DeepSeek Moment, With a Twist

Markets treated K3 as a macro event, not a product launch. Taiwan Semiconductor fell 7% on Friday despite reporting a 77% jump in quarterly operating profit hours earlier; SoftBank, widely traded as an OpenAI proxy, dropped 9%; and Z.ai — the Chinese rival behind the GLM models — plunged almost 30% in Hong Kong. An AI-infrastructure selloff already in motion accelerated, on the same logic as the original DeepSeek shock of early 2025: if frontier capability can be reached without frontier-scale American compute budgets, what exactly is all that capex buying?

The twist is who got hurt worst. In January 2025, DeepSeek’s shock hit American chip stocks. This time the sharpest single-name damage landed on Moonshot’s own domestic competitors — the labs whose entire pitch was being nearly-as-good for much less. K3 compressed them from both directions at once: better than their models, and open enough to erase their differentiation the moment weights ship. There is a lesson in that for every mid-tier lab on earth, Western ones included.

The timeline compression is the other half of the story. Fortune reported that many observers, Anthropic CEO Dario Amodei among them, had not expected a Chinese lab to reach this level for roughly another six months. Whether or not you think benchmark parity equals practical parity, the expectations gap itself moves capital. And it is worth separating two things markets tend to blur: K3 is bearish for the assumption that compute spending alone preserves a capability lead, but it says nothing bearish about AI demand. If anything — as the next section argues — it is the strongest demand signal of the year.

The Real Question: Do Cheap, Open Models Mean More AI Applications — or Fewer?

Strip away the geopolitics and the stock moves, and K3 forces the question every founder, developer, and investor actually cares about: when frontier-class capability becomes a downloadable commodity, does the ecosystem above it expand or contract? This is not an idle debate. If proliferation means more applications, it means more startups, more competition for attention, more infrastructure demand, and more churn. If it means consolidation into a few giant assistants, most of the current AI startup landscape is walking dead. Both positions have serious evidence. Let us take them in turn.

The case for more: Jevons economics and the token data

The strongest argument for expansion is that we have run this experiment continuously for three years and the result has never varied: every collapse in the price of intelligence has increased total consumption, not reduced it. This is Jevons paradox operating in real time. LLM inference prices have been falling at a median of roughly 50x per year depending on the capability milestone — and yet the median enterprise’s monthly LLM bill grew 7.2x year-over-year entering 2026. Prices divided by fifty while spending multiplied by seven: that is not a market being satisfied, it is a market discovering how much intelligence it can absorb. OpenRouter, the largest neutral routing layer, watched its weekly volume grow from roughly 5 trillion tokens in April 2025 to more than 20 trillion a year later.

The open-weight cohort specifically is where that demand is flowing. Chinese open models went from under 2% of OpenRouter traffic in late 2024 to roughly 61% of top-ten token volume by early 2026; the combined share of US models fell from about 70% to about 30% in twelve months. Even inside US enterprises — the most compliance-constrained buyers on earth — Chinese-origin models hit a weekly peak of 46% of routed enterprise tokens by mid-2026, up from 4.5% a year earlier, on price advantages OpenRouter’s own team pegs at 60–90%. Meanwhile the average enterprise now runs 4.2 models in production, up from 1.9 in 2023. Nobody standardizes on one model anymore; they route. Every new capable, cheap option slots into that routing fabric almost frictionlessly.

Open weights add a second, structural argument: they enable kinds of differentiation that closed APIs forbid. A company building on a closed frontier API cannot fine-tune the frontier, cannot own its margin, cannot guarantee the model it built on will exist next quarter. With K3-class weights under a Modified MIT license, a startup can distill, specialize, self-host, and turn the model into a component rather than a landlord. That is not theoretical — it is already how the American AI industry quietly operates. Cursor used Kimi models in building its Composer 2 coding agent; DoorDash’s CTO says the company delegates lower-level work to Kimi K2.6; Thinking Machines used K2.5 to generate post-training data for its own model. Open Chinese models are load-bearing infrastructure inside marquee US startups today. Frontier-class open weights extend that pattern upmarket, and the capital markets are betting accordingly — enterprise agent spending is forecast to reach roughly $1.4 trillion by 2027.

One more distinction does a lot of quiet work here. The force that kills applications is closed-model capability absorption — the frontier assistant swallowing your product as a feature. The force that spawns applications is open-weight availability — raw capability anyone can shape. K3 is unambiguously the second force. It hands ammunition to the long tail rather than the incumbents, because the incumbents already had frontier models; the long tail just got one it can own.

The case for fewer: absorption, wrapper death, and the graveyard data

The bear case deserves a fair hearing, because parts of it are empirically solid. First, the absorption dynamic is real: general-purpose assistants keep eating categories that used to be startups — writing aids, search wrappers, basic research tools, simple coding helpers. Each capability jump at the frontier converts some number of independent products into features. If you believe assistants ultimately absorb most workflows, then more capable models — open or closed — just accelerate the funeral.

Second, building more things is not the same as building more viable things. The execution data is brutal: roughly 88% of enterprise agent pilots never reach production, Gartner expects more than 40% of agentic AI projects to be canceled by the end of 2027, and about 22% of deployed agents show negative ROI at twelve months. Lowering the barrier to entry when the failure rate is this high mostly produces a taller pile of failures. And when the core input is a commodity anyone can download, classical economics says margins get competed toward zero — more applications, none of them worth much.

Third, K3’s own pricing cuts against the cheap-abundance narrative. The best open model on earth just priced itself like a closed flagship. If leading open labs can charge frontier rates during exclusivity windows, the open discount may narrow over time rather than widen. Finally, friction is real: Chinese-origin models carry data-governance and geopolitical baggage that gives many Western enterprises pause, and export-control actions have already disrupted model availability in both directions this year. A bifurcated market is a smaller market for everyone building in it.

Weighing it: the usage data wins

Put the two cases side by side and the asymmetry is hard to miss. The bear case is built mostly on failure rates and plausible futures; the bull case is built on observed consumption. Pilots failing at 88% while aggregate token spend grows 7.2x is not a contracting market — it is a Cambrian market, where enormous mortality and enormous expansion coexist because the cost of attempting things collapsed. The 12% of pilots that survive are being selected hard, and they scale onto ever-cheaper substrate. Every measurable series — tokens routed, models per enterprise, share flowing to open weights, dollars committed to the agent layer — points the same direction, and has for three consecutive years.

So the honest answer is: more applications, with a catch. The catch is that each individual application becomes less defensible, because everyone is drawing from the same ambient pool of capability. Which brings us to the question of where the value actually goes.

Winners and Losers: Where Value Migrates When Models Commoditize

One of the sharper analyses of the open-weight shift makes the point in a sentence: the margin now lives above and below the model, not in it. When the same weights are available to everyone, the model stops being the product and becomes the substrate. Value migrates to whoever controls the layers around it — and K3’s launch is about to demonstrate this in fast-forward.

Start below the model, at the serving layer. July 27 is effectively a starting gun: the moment K3’s weights hit Hugging Face, every serious inference provider will race to announce day-one hosting, and the competition will be fought on price, latency, quantization quality, and reliability — on identical weights. This is a genuinely new kind of market, one where “same model, different serving” becomes a real purchasing decision, and it is a market that grows with every major open release. The routing layer above it wins for the same reason: OpenRouter’s traffic quintupled in six months and the company raised $113 million precisely because a many-model world needs a switchboard. Multi-model is no longer a hedge; per the enterprise data above, it is the default architecture.

Above the model, the winners are applications with assets a downloadable file cannot replicate: proprietary data, embedded workflow position, regulatory approvals, brand, and distribution. Hardware and edge players win too — a permissively licensed frontier model is a gift to anyone selling the boxes it runs on. And the largest winner, as always with commoditization, is the buyer: every company consuming intelligence just watched its input costs get another structural push downward.

The losers list is just as instructive. Mid-tier closed labs are in the kill zone — priced above open alternatives, performing below the frontier, differentiated by neither. The market said this out loud on Friday when Z.ai lost nearly a third of its value in a day. Thin wrappers whose entire product is a prompt on someone else’s API lose next, since their input is now everyone’s input. And a subtler casualty: benchmark marketing as a strategy. When half a dozen labs can credibly claim frontier-adjacent scores, bar charts stop converting. What replaces them, for both models and applications, are the older moats — distribution and trust. Those are about to become the two scarcest assets in AI, which is a theme we will return to in a moment.

There is a practical corollary here for anyone running go-to-market at an AI company. A wider field of credible products fighting over a fixed pool of developer and buyer attention means customer acquisition costs rise even as model costs fall — the savings on the input side get spent on the distribution side. Expect marketing budgets across the AI industry to climb as a share of total spend, expect launch windows to compress as release cadence accelerates, and expect the channels that can actually deliver qualified AI-native audiences to become contested territory. When product differentiation thins, the fight moves to whoever can be seen, understood, and believed first — and that fight is only getting more expensive.

The Second-Order Effects Nobody Is Pricing In

Three downstream consequences of K3-style proliferation deserve more attention than they are getting.

Churn becomes a permanent tax

Faster model cadence means faster model death. Moonshot itself is the case study: alongside K3’s launch, the company closed kimi-k2.5 and the entire legacy moonshot-v1 series to new users and scheduled a full platform sunset for August 31 — weeks after the new flagship shipped, and only months after the original K2 line was discontinued in May and kimi-latest in January. Anyone running production traffic on those models now faces a forced migration with real breaking changes: K3 fixes sampling parameters server-side, supports only maximum reasoning effort, and bills output at multiples of its predecessor’s rate. Every lab is converging on this cadence. Open weights soften the blow in principle — you can keep serving a deprecated model yourself forever — but only if you are the kind of organization that can operate 700 gigabytes of accelerator memory. For everyone else, model churn is now a line item, and tracking who is deprecating what has become genuine operational intelligence. It is a growing part of what we track on the Kingy Launch Radar, because launch coverage without retirement coverage is half a story.

The flood makes trust the scarce good

Here is the uncomfortable corollary of near-free frontier capability: the cost of producing content, reviews, benchmarks, launch pages, and entire competitor products is heading toward zero — which means the volume of all of them is heading toward infinity. Leaderboards get gamed, launch feeds get spammed, AI-written reviews of AI products review each other into a hall of mirrors. When generation is free, the average unit of signal is worth less, and the premium on verified, methodology-backed evaluation rises in direct proportion. This dynamic is exactly why we invested in a validation-first scoring pipeline — the reasoning is laid out in Kingy Score v2 — and why we expect independent evaluation, disclosed methodology, and auditable claims to become the dividing line between AI media that survives the flood and AI media that becomes part of it.

Machines start doing the choosing

The third shift is quieter. As agents take over more selection decisions — which library to install, which API to route to, which tool to recommend — discovery itself becomes machine-mediated. An agent evaluating “which model should handle this workload” does not watch launch keynotes; it reads structured data, pricing endpoints, and changelogs. In a world of hundreds of viable open models, the winners of distribution may increasingly be whoever is most legible to machines, not just most visible to humans. That is a channel most AI companies have not even begun to optimize, and it compounds the previous point: machine-readable trust data only works if someone trustworthy is producing it.

The Bear Case: What Could Break This Thesis

Intellectual honesty requires naming the scenarios under which the expansion thesis fails, and there are four serious ones.

First, consolidation could still win. If frontier assistants keep absorbing workflows faster than open weights spawn new applications, the application layer hollows out and the market concentrates into a handful of super-apps. Current usage data points the other way, but absorption is a step function — one sufficiently general agent release could delete whole categories at once.

Second, the economics of open-weight training remain genuinely unresolved. Frontier runs cost hundreds of millions of dollars; giving away the resulting artifact while third parties compete away your serving margin is a strange business unless something else pays — cloud attach revenue, a strategic patron like Alibaba, state-adjacent motivations, or the exclusivity-window pricing K3 is pioneering. If none of those prove durable, the open-frontier faucet could slow, and this entire ecosystem is downstream of it staying open.

Third, geopolitics could bifurcate the market. Chinese-origin models already face data-governance scrutiny, procurement restrictions, and export-control crossfire — and access disruptions in 2026 have cut in both directions, hitting American flagship models for some users too. A world of walled regional AI stacks is a world where every model’s addressable market shrinks, and where enterprise adoption of the cheapest capable model stalls on legal rather than technical grounds.

Fourth, there is the safety overhang. Open weights at genuine frontier capability are irreversible in a way API access is not: safeguards can be fine-tuned away, and there is no recall button. Reasonable people disagree about where the risk threshold sits, but regulators may not wait for consensus — and a sharp regulatory response to an open-weights incident is the kind of event that could reprice this entire trend overnight. None of these four risks is the base case. All of them are live.

What to Watch Next

The K3 story has five dated checkpoints worth calendar entries:

- July 27 — the weights. Do they land on schedule, complete, and under the promised Modified MIT terms? The license text and any usage conditions deserve a close read, because “open” spans a wide spectrum.

- Early August — the real price. Watch what third-party inference providers charge for K3 in the first weeks of hosting. That number, not Moonshot’s $3/$15, is K3’s true market price — and the speed of its decline is a live measurement of how fast open-weight margins erode.

- August 31 — the sunset. Moonshot retires kimi-k2.5 and the moonshot-v1 series. Watch how forced migrations of production workloads actually go; it is a preview of life at permanent high cadence.

- The Western response. Whether US labs answer with price cuts, their own open releases, or regulatory pressure will say a great deal about which moats they believe they still hold.

- The next escalation. DeepSeek, Qwen, and MiniMax will not sit still — MiniMax was already building its own 2.7-trillion-parameter open model before K3 landed. The trillion-scale open race now has multiple entrants and a two-week news cycle.

The Bottom Line

Kimi K3’s significance was never really the benchmark chart. It is the license attached to the benchmark chart. For the first time, capability within arm’s reach of the absolute frontier is about to be a file anyone can download, specialize, and build a business on — and the evidence of the last three years says the ecosystem will respond the way it always has: by consuming vastly more intelligence, building vastly more things, and killing most of them quickly. More applications, faster churn, thinner moats, cheaper tokens, and a rising premium on the two things proliferation cannot commoditize — distribution and trust. The labs will keep fighting over the frontier. The rest of the economy just got handed the frontier’s hand-me-downs, nine months fresh, and history says that is where the interesting building happens. We will be tracking every step on the Launch Radar and across the Kingy AI tool directory — starting with what actually ships on July 27.

Kimi K3: Frequently Asked Questions

What is Kimi K3?

Kimi K3 is Moonshot AI’s flagship model, launched July 16, 2026. It is a mixture-of-experts system with roughly 2.8 trillion total parameters (16 of 896 experts active per token), a one-million-token context window, native visual understanding, and always-on maximum reasoning, positioned for long-horizon coding and agentic work.

How much does Kimi K3 cost?

API pricing is $3.00 per million input tokens ($0.30 for cached input) and $15.00 per million output tokens, flat across the full context window. Consumer access comes via Kimi subscription plans running roughly $19 to $199 per month, with context limits tiered by plan.

Is Kimi K3 open source?

Strictly, it is open-weight rather than open-source: Moonshot has committed to releasing the full model weights on Hugging Face by July 27, 2026 under a Modified MIT license permitting commercial use, but training data and full training code are not published. Until the weights land, K3 is API-only.

How does Kimi K3 compare to Claude Fable 5 and GPT-5.6?

By Moonshot’s own account, K3 trails Claude Fable 5 and GPT-5.6 Sol on overall capability while matching or beating them on several coding and agentic benchmarks. Independent early rankings place it roughly fourth among all models — the strongest open-weight system ever released, just below the closed frontier leaders.

Can I run Kimi K3 locally?

Only with serious infrastructure. At 2.8 trillion parameters, even aggressive quantization implies roughly 650 GB to 1 TB of memory before serving overhead. Realistic self-hosting is the domain of inference providers, large enterprises, and well-funded teams — most users will access K3 through APIs or hosted providers.

Which Kimi models are being retired?

Following the K3 launch, kimi-k2.5 and the legacy moonshot-v1 series are closed to new users, with a full platform sunset on August 31, 2026. The original K2 line was discontinued on May 25, 2026, and kimi-latest in January — so production workloads on older Kimi models should plan migrations now.