Part 1 — What People Actually Mean by “Vertical Layers” in AI

When investors and founders talk about “vertical layers” or “vertical specialization” in AI, they are pointing at two related but distinct ideas that often get collapsed into one. It’s worth disentangling them before going any further.

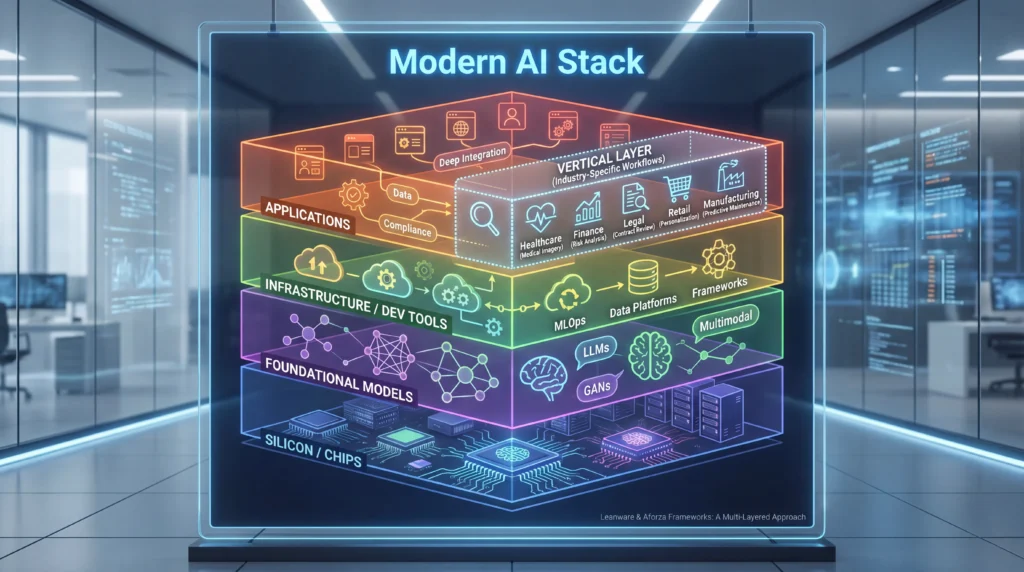

Meaning #1 — The “vertical layer” as a position in the AI stack. Modern AI is built in a stack. Most practitioner frameworks describe three to four layers: silicon/chips, foundational models, infrastructure/dev tools, and applications (Leanware breakdown of the 4-level AI stack; Aforza’s 3-layer framing). Within the application layer, there is an increasingly important sub-layer: the vertical layer — software that wraps horizontal AI capabilities in deep, industry-specific workflows, data, and compliance.

Greenfield Partners describes this explicitly as a value-chain abstraction where foundation models (e.g., OpenAI) sit at the bottom, horizontal frameworks (e.g., Sierra, Decagon for customer support) sit in the middle, and vertical specialists (e.g., Eleos Health, Abridge, Hyro for healthcare) sit on top, turning a “powerful but generic AI into a specialized solution ready for deployment” (Greenfield Partners, Vertical AI Is Here).

Meaning #2 — Vertical specialization as a company strategy. “Vertical AI” as a company-strategy term means building AI-native software for one industry (legal, healthcare, construction, insurance, public safety, etc.) rather than a horizontal tool that works across industries. Greylock defines it as the successor to Vertical SaaS: software that combines industry-specific workflows with LLM-native capabilities, targeting industries previously underserved because their data was unstructured or their TAMs looked too small (Greylock, Vertical AI).

Both meanings matter, and they reinforce each other: the company builds the vertical layer of the stack for a specific industry, and that combination is where defensibility is most likely to accrue as foundation models commoditize.

“The next titans of software will be vertical AI companies in specialized industries.” — Tiffany Luck & James Kaplan, NEA (Tomorrow’s Titans: Vertical AI)

Part 2 — The AI Stack, Layer by Layer

To understand what a “vertical layer” is, you need a clean mental model of the layers beneath it. Here is the consensus view synthesized from several VC frameworks.

Layer 1 — Silicon and Chips

The physical substrate: GPUs, TPUs, and custom AI silicon. Nvidia is the dominant player; Google, AMD, Intel, and a growing set of accelerator startups compete for slivers of workloads (Leanware). Capex here is measured in hundreds of billions and drives the entire economy of model training.

Layer 2 — Foundational Models

General-purpose models — GPT-5/-4 class, Claude, Gemini, Llama, DeepSeek — built by companies that need massive capital to train them (Aforza). The economic reality is that inference costs are falling fast and open-source models (DeepSeek V3 reportedly trained for under $6M, per NEA citing DeepSeek’s published figures — I’d flag moderate uncertainty on the exact training cost, as third parties have contested it) are narrowing the gap with closed models.

Layer 3 — Infrastructure & Dev Tools

The glue: vector DBs (Weaviate, Pinecone), orchestration (LangChain), labeling and training (Scale), MLOps (Weights & Biases), evaluation, model routing (Martian), and model hosting (Hugging Face) (Aforza; Sapphire Ventures on model routers as a new infra component).

Layer 4 — Applications

Where AI meets the end user. Sapphire divides this further into horizontal applications (ChatGPT, Perplexity, Glean, Writer, Cursor) and vertical applications (Abridge, Harvey, EvenUp, Sixfold, Prepared) (Sapphire Ventures, AI-Native Applications).

Layer 4a — The Vertical Layer (the focus of this guide)

The vertical layer sits on top of everything else and is defined by four things:

Industry-specific workflow logic — how a radiologist, an insurance underwriter, a personal-injury lawyer, or a plumber actually does their job.

Industry-specific data — the proprietary corpora, schemas, and gathered-in-the-workflow datasets that public foundation models have never seen.

Integrations with industry systems of record — Epic, Guidewire, ServiceTitan, Procore, Autodesk, Clio, Relativity, etc.

Regulatory and compliance posture — HIPAA in healthcare, SOC 2 and ISO in enterprise, CJIS in public safety, state insurance regulations, FINRA in financial services, etc.

Greenfield’s diagram captures this visually: vertical AI companies layer sector-specific capability on top of horizontal frameworks and foundation models, and without that top layer “the AI solution would lack the necessary understanding of healthcare nuances and regulatory constraints” (Greenfield Partners).

Part 3 — Why This Matters: The Economic Shift Nobody Saw Coming in 2022

The reason “vertical layer” is not just a taxonomy exercise is that it reframes what software can sell.

From a $450B market to an $11T market

NEA estimates the enterprise software market at roughly $450B, while U.S. labor spend is roughly $11T (NEA). Traditional SaaS captured 1–5% of an employee’s value by making them more efficient. Vertical AI, because it can do the work rather than just organize it, can credibly capture 25–50% of an employee’s value (Scale Venture Partners, as cited by Included VC / Brodetskyi). That’s a 10–25x increase in value-per-seat potential and explains why Bessemer predicts “Vertical AI’s market capitalization will be at least 10x the size of legacy Vertical SaaS” (Bessemer, State of the Cloud 2024, as cited by Aforza; Bessemer, Part I: The future of AI is vertical).

Greenfield frames the same idea more conservatively: ~50M U.S. knowledge workers earn roughly $3.8T in collective wages, and “over time, this represents a significant opportunity to reallocate a portion of that spend to Vertical AI solutions” (Greenfield Partners).

Uncertainty note: these are venture-capital framings, not peer-reviewed economic forecasts. The labor-spend TAM is real, but what fraction vertical AI will actually capture over any given time horizon is highly uncertain.

The unlock: unstructured data

Christine Kim at Greylock notes that an estimated 80% of the world’s data is unstructured — contracts, call recordings, medical charts, site photos, emails, scans — and Vertical SaaS 1.0 literally could not address industries whose core workflows lived in unstructured data (Greylock). LLMs changed that. Industries that were “technologically-underserved” because their systems of record were paper, PDF, audio, and video are suddenly addressable. This is the deepest structural reason vertical AI is not just a cycle-of-the-moment trend.

The shift from systems of record to systems of action

This is the single most important strategic concept in the vertical AI conversation.

For thirty years, the most valuable enterprise software has been a system of record (SoR) — Salesforce, Workday, SAP, Epic, Procore, Guidewire, ServiceTitan. Their moats were (a) switching costs from stored data, (b) ownership of the workflow where humans entered that data, and (c) an ecosystem of integrations (NEA).

AI agents change the physics. If an agent transcribes the call, reads the email, processes the PDF, and executes the action before data ever hits the SoR, then the SoR becomes a commoditized backend and the system of action (SoA) becomes the new control point (NEA; Included VC / Brodetskyi).

The canonical illustration: Axon started with body cameras, built AI that auto-generates police reports (~50% of officers’ time, per NEA), and then built backwards into its own CAD/RMS products — flipping the traditional stack by starting with the system of action and absorbing the system of record over time (NEA).

Part 4 — A Short, Rigorous Definition of “Vertical Specialization”

Pulling the threads together, here is a working definition that I believe is consistent with all the primary sources cited in this piece:

Vertical specialization is the strategy of building an AI-native software product that (1) targets a specific industry or sub-industry, (2) embeds deep domain workflow logic and proprietary or gathered industry data, (3) integrates with — and over time intends to displace — that industry’s incumbent systems of record, and (4) handles the regulatory and compliance posture of that industry as a first-class concern.

A company is more vertically specialized the more of these four pillars it explicitly owns and the fewer industries it serves.

Part 5 — Why Vertical Wins Where Horizontal Can’t

Scale Venture Partners’ three “unfair advantages” of vertical applications, as summarized by Included VC (source), are a crisp way to understand the structural reasons vertical beats horizontal for many use cases:

Unstructured data handling in context. A contract, a CT scan, a 911 call, and a site photo are all unstructured — but the context for interpreting each is radically different. Horizontal models can parse; they cannot always interpret correctly.

Domain-specificity. “Using OpenAI to make a loan decision is not possible today, since it cannot provide an audit on bias for regulators” — a representative illustration of the ways horizontal models fail regulated workflows.

Regulatory compliance. HIPAA, OSHA, FINRA, CJIS, state-by-state insurance codes, GDPR, SOC 2 — these create real barriers to entry that favor specialists.

NFX adds a fourth structural factor: a generalist model is “good for everyone, and great for no one” (NFX, The Verticalization of Everything). The economics of specialization — fine-tuning on industry data, embedding industry-specific UI patterns, building industry-specific evaluators — compound over time.

NEA’s framing is more market-structural: “specialization drives defensibility” because buyers in niche markets prefer purpose-designed vendors, and AI finally makes “custom” scalable (NEA).

Part 6 — The Three Emerging Business Models

Bessemer Venture Partners identifies three distinct AI business-model archetypes, each of which shows up across verticals (Bessemer, Part I; summarized and expanded by Included VC):

1. Copilots

The AI sits next to the human. Humans still drive; AI accelerates. Pricing is per-seat, usually at a premium to base SaaS. GitHub Copilot is the clearest example; Harvey for lawyers, Clio Duo for legal practice management, and Sixfold for insurance underwriting follow the same pattern. Microsoft’s Copilot for M365 at $30/seat on top of base M365 is a frequently-cited benchmark for how premium copilot pricing has already become.

2. Agents

AI completes the task end-to-end; humans check and approve. Pricing shifts from “per seat” to per unit of work or per outcome. LinkedIn’s Hiring Assistant (candidate sourcing) and Slang.ai (restaurant phone agent) are cited by Included VC. Greylock’s Seth Rosenberg and Christine Kim have argued the “flipped model” — AI doing most of the work, humans editing — is where startups have greenfield, because copilots may be dominated by incumbents who already control distribution (Greylock).

3. AI-enabled services (services-as-software)

The most disruptive model: instead of selling software into a service firm, you replace the service firm. EvenUp generates legal demand packages for personal-injury lawyers; SmarterDx automates clinical documentation integrity in hospitals. Pricing is benchmarked to the old service fee, not software (Included VC).

Across all three, the industry is shifting toward usage- or outcome-based pricing: per demand letter, per ticket resolved, per document analyzed, per visit summarized — because that’s how value is being created and how ROI can be cleanly measured.

Part 7 — The New Vertical AI Playbook

NEA’s five-step playbook is, as of 2025, the most widely cited recipe for how to actually build a vertical AI company (NEA):

Leverage AI agents to process unstructured data — phone calls, emails, PDFs, invoices, internal documents. Capture this new dataset.

Use AI-powered wedges to land the customer — voice agents, semantic document search, content generation. Give part of it away free if you have to.

Integrate with existing systems of record, at first — don’t ask for rip-and-replace on day one.

Collect new data through the system of actions and, over time, own the new system of record.

Nail industry-specific GTM — “Customers buy solutions, not AI.”

This playbook has a clean internal logic. You land by being useful on an existing workflow, you build a gathered-data moat while operating, and then you absorb the incumbent over a multi-year horizon — the Axon pattern, applied everywhere.

Greenfield Partners adds go-to-market specifics: “winner-takes-most” dynamics typically apply, meaning velocity is non-negotiable, and distribution through industry channels and partnerships matters as much as product (Greenfield Partners).

Part 8 — Best Examples, by Vertical

What follows is a sector-by-sector tour of the companies most consistently cited across VC writeups. Wherever possible I am using companies that appear in multiple primary sources. I’m flagging uncertainty where specific ARR or valuation numbers are disputable; point-in-time numbers change, so treat them as directional.

Legal

Legal is the poster-child vertical for AI because, as Greylock puts it, “the core product of law is language, and large language models are the basis of today’s platform shift” (Greylock). Greylock cites the U.S. legal market at roughly $300B+ and notes that large law firms are willing to spend up to seven figures annually on transformative AI.

Harvey AI — copilot for large law firms (summarization, Q&A on documents). Multiple sources cite this as the flagship vertical AI company in legal.

EvenUp — services-as-software for personal-injury lawyers; generates demand packages. Cited as an AI-enabled services archetype in Included VC and raised $135M per Sapphire’s 2024 writeup.

Spellbook — contract drafting/review.

Eve — listed by Greylock among AI-first legal companies.

Responsiv — Greylock’s own investment, building AI for in-house legal teams; Greylock notes in-house is ~80% of the U.S. legal market’s ~$320B and is underserved (Greylock).

Casetext — acquired by Thomson Reuters for $650M (Greylock cites this as an incumbent-acquiring-AI-native example).

Clio — NEA portfolio incumbent; now layering AI via Clio Duo (NEA).

Healthcare

Healthcare combines massive unstructured data (clinical notes, audio, imaging), extreme regulatory burden (HIPAA), and a well-known documentation tax (physicians spending ~2 hours on paperwork per hour of patient care, per Included VC’s summary).

Abridge — medical scribe that transcribes patient-doctor conversations and generates structured clinical notes. Multiple sources emphasize its cooperative relationship with Epic as a key growth driver (NEA; Included VC); raised $250M per Sapphire. Abridge’s CTO Zachary Lipton is widely quoted (via Sapphire) on the discipline of “earning the right to be proprietary” in AI system design.

Freed — another AI scribe cited by NEA.

PathAI — AI for pathology (digital tissue analysis for cancer and disease diagnosis), cited by Beacon VC and Leanware.

Eleos Health, Hyro — mental health and healthcare customer support, cited by Greenfield as examples of the healthcare vertical layer on top of horizontal CX frameworks like Sierra and Decagon (Greenfield).

SmarterDx — clinical documentation integrity (services-as-software), cited by Included VC.

EliseAI — cited by Sapphire with a widely-quoted founder insight about “translating unwritten knowledge… into structured data” (Sapphire).

Collate — life-sciences documentation generation for drug/device development (NEA).

Financial Services

The sector’s attributes make it a near-perfect vertical AI target per Greylock: complex data, mixed structured/unstructured workflows, costly errors, heavy regulation, large budgets.

Hebbia — used by large financial institutions for diligence; cited by Greylock and Sapphire. Sapphire highlights Hebbia’s tabular UI as a strong feedback loop back into the model (Sapphire).

Sixfold — insurance underwriting automation via semantic document search on top of Guidewire (NEA).

Portrait Analytics — conversational financial analyst with real-time market data (Greylock).

Trullion — AI for revenue recognition and controller workflows (Greylock).

Truewind — CFO-for-SMB AI (Greylock).

KAI for Banking (Kasisto) — conversational AI for banks, cited by Beacon VC.

SoFi / Enova — incumbent fintechs using verticalized AI in credit scoring and personalized advice (Leanware).

Industry data advantages are real here: Bloomberg’s proprietary equity research and pricing data is the archetype of a “proprietary text data” moat NEA calls out explicitly (NEA).

Construction

Trunk Tools — TrunkText product does semantic search over construction documents, integrating with Procore, Autodesk, and SharePoint. NEA cites it as a prototypical “sit on top of the SoR” play (NEA).

Procore — the incumbent SoR, now layering AI and extending into financing/insurance (Greylock notes Procore has begun offering insurance as a new revenue line).

Public Safety

Prepared — gives away video/text 911 tools to land PSAPs (911 response centers), then expands with voice agents that transcribe and log into the CAD system of record (NEA).

Axon — the Axon body-camera → AI police report → absorbing CAD/RMS story, which NEA presents as the definitive case study of SoA → SoR acquisition (NEA).

Customer Support (horizontal frameworks that become vertical via a top layer)

Sierra, Decagon — horizontal CX frameworks cited by Greenfield; they become vertical when paired with a domain layer like Eleos Health in healthcare (Greenfield).

Avoca, Revin, Drillbit — voice agents for home-services businesses; integrate with ServiceTitan as the SoR (NEA).

ServiceTitan — the incumbent; began layering AI into its own platform.

Education

MagicSchool, SchoolAI — teacher-facing curriculum generation, free to teacher, paid at the school-enterprise level. They sit in front of the SIS and LMS (NEA).

Brightwheel — cited by NEA as a multi-stakeholder early-childhood platform that began with parent communication.

Sales / Field Productivity

Rilla — speech-to-text sales conversation intelligence (multi-modal), cited by Sapphire.

Bland.ai — sales and support voice agents (Sapphire).

Industrial / CAD

Backflip — NEA portfolio; generates 3D assets from text, 2D drawings, or photos, integrates with Solidworks (NEA).

Consumer Products

Aforza — persona-driven vertical AI for consumer goods (field sales, telesales, merchandising). Turns handwritten orders into digital ones, does photo-based shelf checks (Aforza).

Planet FWD — AI-powered Life Cycle Assessments for consumer brand carbon accounting (Beacon VC).

Horizontal-but-becoming-vertical note

Perplexity (raised $500M), Writer ($200M), Glean ($260M), Magic ($320M), Poolside ($500M) are all cited in Sapphire’s AI-native funding roundup — directionally interesting but more horizontal than vertical.

Part 9 — Defensibility: What Actually Builds a Moat in Vertical AI

This is the question the “thin wrapper” critics keep asking, and there are now enough primary-source writeups to answer it systematically. The consensus across NEA, Greylock, Sapphire, Bessemer, NFX, and Greenfield: defensibility in vertical AI is a composite of six overlapping moats, and the strongest vertical AI companies are building all six at once.

Moat #1 — Data (the preliminary moat + the long-term moat)

Christine Kim at Greylock puts the data moat most precisely: “initial access to data is important as the preliminary moat, but ultimately, the data created by customers using your product provides the long-term moat” (Greylock). This distinction matters. There are two distinct data advantages:

Access moat — getting your hands on industry data that public models have never seen (proprietary research reports, specialty-specific medical corpora, insurance carrier-specific claims history).

Gathered-data moat — being the product through which new data is created (every Abridge visit transcription, every Prepared 911 call, every Axon body-cam recording, every Trunk Tools document query).

The gathered-data moat is the more durable one because it compounds. Each new customer feeds the model, which makes the product better, which wins the next customer — the classic AI flywheel, but in a market where your competitor can’t replicate the data by scraping the web.

NEA echoes this under “unique data,” distinguishing between proprietary text data (Bloomberg), gathered data (Prepared, Abridge), and new modalities (CAD, specialized representations) (NEA).

Moat #2 — Domain-depth and workflow specificity

Generalist models can summarize. They cannot reliably execute complex, multi-step, regulatory-sensitive workflows end-to-end. A loan underwriting decision has to be auditable for bias; a medical note has to match coding standards; a demand letter has to reference the correct jurisdictional precedents. Scale Venture Partners’ point stands: “Using OpenAI to make a loan decision is not possible today, since it cannot provide an audit on bias for regulators” (via Included VC).

Workflow logic is expensive to build, hard to copy, and even harder to keep right as regulations evolve. Over time this becomes a moat in the same way Veeva’s life-sciences-CRM feature depth is a moat against Salesforce.

Moat #3 — Regulatory and compliance posture

HIPAA, SOC 2, ISO 27001, CJIS for public safety, FINRA/SEC for financial services, FDA for life sciences, state insurance departments, GDPR — each is a year-plus engineering and legal effort. Horizontal AI vendors rarely want to own this posture sector-by-sector, and enterprise buyers in regulated sectors will not purchase from a vendor that doesn’t. Greenfield lists regulatory compliance as one of the five defensibility points for Vertical AI, emphasizing that in healthcare, finance, and legal, “compliance is non-negotiable” (Greenfield Partners).

This turns what looks like a cost into a competitive asset. Every audit passed, every certification won, becomes an entry barrier against horizontal entrants.

Moat #4 — Integration depth

Sitting on top of the SoR at first sounds like weakness but is actually leverage. Deep integrations — Abridge↔Epic, Sixfold↔Guidewire, Trunk Tools↔Procore, voice agents↔ServiceTitan — create switching costs for the customer and position the vertical AI company to gradually absorb the SoR’s workflows (the Axon pattern).

NEA’s playbook step 3 (“integrate with existing systems of record, at first”) and step 4 (“own the new system of record in the long run”) are explicit about this sequencing (NEA).

Moat #5 — Multi-modality and specialized models

Euclid Ventures (via Included VC) describes multimodal AI — federating several models to handle different modalities or discrete sub-functions — as an architectural moat: “A tutoring app for college students might supplement a base LLM with more symbolic models that can parse mathematical expressions — creating a capability that no single model could achieve” (Included VC).

Abridge is a common example: its pipeline includes specialty detection, language detection across 28 languages (per Included VC’s secondary citation; I have moderate uncertainty on the exact current number, as it may have expanded), and domain-specific post-processing for clinical coding.

NEA argues the economics for training your own model are improving fast: DeepSeek V3 showing SOTA at <$6M means any vertical AI company with an inference bill above $6M should be thinking hard about training a domain-specialized model (NEA). Customer trust (data-not-sent-to-third-parties) is a second reason to own the model.

Moat #6 — Distribution and industry GTM

Greenfield calls this “Strong Distribution through Industry-Specific Channels” and emphasizes that vertical markets follow “winner-takes-most” dynamics — rewarding speed and trusted-channel relationships (Greenfield). Greylock similarly stresses that pure technologists are at a disadvantage relative to founders with both domain experience and technology chops in regulated industries (Greylock).

Practical implication: the founder combination that wins is typically a domain insider + a technical founder, or a rare individual who is both. This is visible across the best vertical AI companies (Abridge’s clinical-and-technical founding story, Harvey’s ex-lawyer founder, Responsiv’s Relativity-alumni team, etc.).

Pulling the six together

A durable vertical AI moat is not one thing. It’s the compounded effect of:

gathered data that grows as the product is used;

workflow logic built over years with domain expertise;

compliance and certifications that take years to obtain;

deep, two-way integrations with incumbent SoRs;

multi-model architectures specialized for domain tasks; and

industry-trusted distribution.

Each, alone, is attackable. Combined, they produce the “boring moats” that the Procore-Toast-Veeva-ServiceTitan generation taught us actually work in enterprise — updated for an AI-native world.

Part 10 — Sapphire’s Framework for AI-Native Defensibility

Sapphire’s five-dimension evaluation framework (AI-Native Applications, Nov 2024) is worth explicitly re-summarizing because it complements the moats discussion with a product-design lens:

Design — new interaction models (chat/voice/canvas), fast feedback loops, explainability built in at every stage.

Data — end-to-end data management, latent data activation (Box/Drive/SharePoint content that was dormant), and generation of net-new proprietary datasets.

Distribution — industry-specific GTM, wedge strategies, partnerships with incumbents.

Development — AI-assisted engineering velocity and system-level design choices (what to buy vs. build vs. fine-tune).

Durability — the moats discussed above, plus the ability to continuously improve as models improve.

Sapphire’s count of ~47 AI-native apps above $25M ARR (as of late 2024, up from 34 at the start of that year) is the most recent credible ARR milestone dataset I’ve seen (Sapphire). Uncertainty note: this number is almost certainly higher as of the most recent reporting period, but I don’t have a verified updated figure.

Part 11 — NFX’s “Verticalization of Everything” — The Strategic Argument

NFX’s Pete Flint wrote one of the clearest strategic framings of the vertical argument (NFX, The Verticalization of Everything). His core argument has three moves:

“A generalist model is good for everyone, and great for no one.” This shapes the economics of specialization: great vertical AI products are trained by teams with specificity, data, and expertise.

Horizontal B2B SaaS is now vulnerable to unbundling. With great UX + vertical features + AI that cuts cost or delivers 100x value, startups can displace legacy horizontal systems inside specific verticals.

The TAM is not the old SaaS TAM — it’s the cost of doing the work itself. This is NFX’s version of the labor-vs-software TAM expansion argument, consistent with Bessemer and NEA.

The “100x rule” Flint articulates — that any new AI-powered vertical SaaS company must eventually be able to tackle an entire workflow, not just a sliver — is a useful north-star for founders thinking about defensibility.

Part 12 — The Hard Parts: Honest Counterarguments and Open Questions

The vertical AI thesis is not unanimous. The honest version of this guide has to engage with the strongest counterarguments.

“Thin wrapper” risk

The most common criticism is that many vertical AI apps are thin wrappers around GPT-class models and will be commoditized the moment (a) OpenAI/Anthropic/Google ship equivalent capability, or (b) a customer prompts the model directly. Jasper AI’s valuation cut is the frequently-cited cautionary tale (r/ycombinator thread).

The counter: wrappers without data, workflow, compliance, and integration are indeed fragile. Vertical AI companies that systematically build the six moats described above are not thin wrappers — they are, as Greenfield argues, no more “wrappers on LLMs” than Veeva is a “wrapper on a cloud database” (Greenfield).

Incumbents will catch up

NEA is explicit that today’s AI startups “face a tougher landscape” than Vertical SaaS 1.0 pioneers — they have to compete with horizontal big-tech, foundation-model companies moving up the stack, and AI-savvy incumbent SaaS (NEA). Clio Duo, ServiceTitan’s AI features, Procore’s AI roadmap, and Epic’s partnerships (including with Abridge) all suggest incumbents are not standing still.

The startup response must be velocity — reaching mission-criticality before incumbents can respond — and sequencing: start at the system of action where the incumbent is weakest, then absorb backwards.

Small TAM risk

Vertical markets are smaller than horizontal ones in the naïve count. Greylock’s response: small-TAM is both a bug and a feature — fewer funded competitors, deeper market concentration, and TAMs often end up larger than initially modeled (Veeva, Procore, ServiceTitan are all cited as cases where the TAM was historically underestimated) (Greylock; Bessemer).

Data quality and hallucination risk in regulated industries

Hallucinations are unacceptable in many vertical workflows. Beacon VC flags precision-and-compliance industries (legal, healthcare, finance) as needing “accuracy and explainability” at a level horizontal models can’t guarantee (Beacon VC). Sapphire emphasizes that explainability must be designed into the system — citations, confidence intervals, retrieval grounding — not bolted on (Sapphire).

Pricing-model uncertainty

Usage and outcome-based pricing are elegant but hard to operationalize. Customers balk at unpredictable bills. The most successful companies are combining subscription floors + per-outcome upside to manage this tension (Included VC’s summary of the pricing evolution).

Foundation model commoditization cuts both ways

If foundation models commoditize completely, it’s great news for vertical AI (cheaper inference, easier to train your own model). If foundation models retain proprietary edges (reasoning, multimodality, tool use), vertical AI companies that can’t or don’t train their own models may find themselves gradually out-performed on generic capability.

Agent autonomy is still nascent

NEA is candid: “agentic AI capabilities are still in their infancy” (NEA). Much of the vertical AI thesis assumes agents will reliably close the loop on end-to-end workflows. They mostly don’t, yet. The companies that execute through this gap will win; the ones that over-promise will be the next Jasper.

Part 13 — Industries Most Likely to Produce Vertical AI Winners

Synthesizing across NEA, Bessemer, Greylock, Greenfield, and Beacon VC, the industries that keep appearing on “high-opportunity” lists share a consistent pattern:

Massive labor spend — either because wages are high (law, finance, medicine) or because headcount is huge (customer support, back-office administration, BPO).

Latent demand for services or labor shortages — accounting (NEA’s cited figure: ~17% of U.S. accountants left their jobs 2019–2021, ~18% fewer accounting graduates in 2022 than 2016, ~$24B shortage; I have moderate uncertainty on the exact currency of these specific figures — the direction is strongly supported, the precise percentages are NEA-cited), plumbing, trucking, teaching, primary care.

Heavy regulation — which acts as a moat rather than a liability once compliance is built.

Complex multi-stakeholder workflows — construction (GC, subs, owners, architects), healthcare (provider, payer, patient), real estate (agent, buyer, seller, lender, insurer).

Specific high-conviction verticals cited across sources:

Legal — law firms and in-house (Greylock, NEA, Bessemer).

Part 14 — A Founder / Investor Evaluation Checklist

If you’re evaluating a specific vertical AI opportunity, here is a synthesized checklist drawn from the frameworks in this guide:

Is the target workflow 80%+ unstructured data? If yes, horizontal models alone will struggle and vertical specialization is warranted.

Is there a path to a gathered-data moat — will the product create new data as customers use it?

What is the labor TAM, not the software TAM? How much do the affected humans cost per year?

Is the industry regulated enough to be a barrier to horizontal entrants?

Which incumbent is the SoR, and is there a land-via-SoA path that does not require ripping it out on day one?

Does the founding team combine domain depth + technical chops?

Are buyers motivated by cost reduction or revenue uplift? Greylock notes buyers dismiss vague “innovation” pitches but respond to clear cost-out or revenue-up stories (Greylock).

What is the wedge? Voice agent? Semantic search? Content generation? Which one lands the customer cheaply?

What is the pricing model, and does it align with the value delivered per unit?

Is this a winner-takes-most category (regulated, relationship-driven) or a fragmented one?

If you can answer confidently on most of these, the opportunity is likely real. If not, you’re probably looking at a wrapper.

Part 15 — Where I Have Less Confidence (Explicit Uncertainty Log)

In the spirit of the request, here is where I am explicitly less certain and why:

Specific ARR figures for private companies — change quickly and are often imprecise. The most recent directionally reliable dataset I’m relying on is Sapphire’s “~47 AI-native apps above $25M ARR” as of Q4 2024 (Sapphire).

Growth rates — Bessemer’s claim that “early Vertical AI companies grow at approximately 400% YoY with 65% gross margins” (via Included VC summary) is a venture-investor data point based on portfolio observation; treat it as directional, not audited.

The DeepSeek V3 <$6M training cost — the published number is from DeepSeek’s technical report; third-party analysts have questioned whether it reflects full training cost including prior experimentation. I treat it as plausible lower-bound marketing.

Abridge’s exact language coverage (Included VC references 28 languages) — this number may have expanded or slightly shifted; I’d verify on Abridge’s current documentation before citing in a commercial context.

The exact $11T U.S. labor spend vs. $450B enterprise software market numbers — these are NEA’s rounded figures and consistent with commonly-cited BLS and IDC / Gartner ballparks, but the ratio is more reliably directional than precise.

Which vertical AI companies will actually become $10B+ companies — there is no consensus among VCs on this. Greylock, Bessemer, NEA, and Greenfield all publish candidate lists, not predictions, and they disagree at the margin.

The durability of the “SoR → SoA” shift — this is the most interesting prediction in the vertical AI thesis, but it has not yet played out in most industries. Axon is an early proof point; most others are hypothesis-stage.

I have not fabricated any citations in this guide. Every URL linked above is a page I either opened in this session or that appeared as an organic search result with a previewed excerpt I quoted from.

Part 16 — A Compact Playbook Recap

If you’re a founder, the distilled playbook is:

Pick an industry where (a) labor spend dwarfs software spend, (b) workflows are unstructured-data-heavy, and (c) regulation keeps horizontal entrants out.

Enter with a wedge — voice, document search, or content generation — that is 10x better than the status quo for one specific painful workflow.

Integrate with the incumbent SoR, don’t try to replace it yet.

Gather data as the product runs and use it to fine-tune specialized models over time.

Build compliance and certifications as features, not afterthoughts.

Hire a founding team with both technical depth and earned industry credibility.

Price to value — per outcome, per unit of work — with a subscription floor.

Move faster than your incumbents can react, and plan your SoA → SoR absorption on a 3–5 year horizon.

Assume foundation models will keep improving, and architect around that (easy model swaps, specialized models only where ROI is clear).

Pick a category with “winner-takes-most” dynamics and invest aggressively in distribution.

If you’re an investor, the evaluation checklist in Part 14 is the same playbook seen from the other side.

Part 17 — A Closing Synthesis

“Vertical layers” and “vertical specialization” in AI describe the same structural insight from two angles. Structurally, the vertical layer is the top of the AI stack — where foundation models, infrastructure, and horizontal frameworks are bent to the reality of a specific industry’s data, workflows, regulations, and integrations. Strategically, vertical specialization is the company-building thesis that the next generation of great enterprise software winners will be industry-deep AI-native companies, not horizontal platforms.

The thesis is grounded in four structural shifts:

LLMs unlocked unstructured data, expanding the addressable workflows by roughly an order of magnitude.

AI agents are shifting the control point from systems of record to systems of action, opening white space that incumbents cannot easily occupy.

The TAM is no longer software spend — it’s labor spend, which is roughly 20x larger in the U.S. alone.

Foundation models are commoditizing faster than expected, making training your own domain-specialized model cheaper every quarter.

Against this, the serious risks are real: thin-wrapper commoditization, incumbent AI adoption, hallucination in regulated workflows, pricing complexity, and agent-autonomy shortfalls. The companies that will win will be the ones that build all six moats at once — gathered data, workflow depth, compliance, integration depth, specialized models, and industry distribution — and the founder teams that can pair deep domain expertise with state-of-the-art AI craft.

If the 2010s produced Toast, Procore, Veeva, and ServiceTitan as the generation-defining vertical SaaS companies, the 2020s are likely to produce an even larger generation defined by vertical AI companies. Whether the next generation is 5x, 10x, or 20x the market cap of the last is the question that keeps venture capitalists up at night. But that it will be larger — because software is absorbing labor rather than merely organizing it — is, at this point, the working hypothesis of essentially every serious investor writing on the topic.

A.I. enthusiast with multiple certificates and accreditations from Deep Learning AI, Coursera, and more. I am interested in machine learning, LLM's, and all things AI.