The data is in, and it tells a story that should reshape how you think about where to put your money in the AI era.

There’s a quiet confidence spreading through a particular corner of the venture capital world. It belongs to the investors who backed enterprise AI — the ones who wrote checks into workflow automation tools, AI-powered CRMs, procurement intelligence platforms, and vertical SaaS companies selling to CFOs and supply chain managers. They’re not the ones making headlines. They’re not the ones whose portfolio companies are on the cover of Wired. But they’re the ones sleeping soundly.

Meanwhile, across town — sometimes literally — the investors who poured money into consumer-facing AI apps are checking their dashboards at 2 a.m. They’re watching churn rates that would make a traditional SaaS investor weep. They’re watching users sign up, play around for a few weeks, and vanish. They’re watching the next shiny model drop from OpenAI or Anthropic and wondering whether their entire portfolio thesis just became obsolete overnight.

This isn’t a story about which technology is more impressive. Consumer AI products are often breathtaking. It’s a story about business fundamentals — about what makes a company durable, what makes revenue sticky, and what makes an investor’s portfolio resilient to the relentless churn of technological change. And on every one of those dimensions, B2B AI is winning.

The Churn Problem Is Real, and It’s Catastrophic for B2C AI

Let’s start with the data, because the data is damning.

In late 2025, analyst Kyle Poyar teamed up with ChartMogul to conduct one of the most rigorous studies of AI product retention ever published. They scraped the websites of 3,500 software companies, used AI to categorize them as B2B SaaS, B2C SaaS, or AI-native, and then compared gross revenue retention (GRR) and net revenue retention (NRR) rates across all three groups.

The results were stark.

B2B SaaS, the old reliable, posted a median NRR of 82%, with the upper quartile reaching 97%. These are companies where customers don’t just stay — they expand. B2C SaaS was considerably worse, with a median NRR of only 49%. But the real shock was the AI-native category. These companies — the ones building on top of large language models, the ones with the flashy demos and the viral Twitter threads — posted a median GRR of just 40% and a median NRR of 48%.

Let that sink in. The median AI-native company is losing 60% of its revenue base every year.

Poyar coined a term for this: the “AI tourist problem.” Buyers sign up because they’re intrigued by the possibility of what AI could do. They haven’t planned for how the product fits into their business long-term. They’re experimenting, not committing. And when the experiment ends — or when a better experiment comes along — they cancel.

The pattern is especially brutal at the low end of the pricing spectrum. According to the ChartMogul data, AI-native products priced below $50 per month see just 23% GRR and 32% NRR. Products priced between $50 and $249 per month see 45% GRR and 61% NRR. Only when you get above $250 per month — which is to say, only when you’re selling to businesses — does retention normalize to something resembling traditional B2B SaaS: 70% GRR and 85% NRR.

The conclusion is almost too clean: the best protection against AI churn is selling to businesses, not consumers.

The “AI Wrapper” Trap

To understand why B2C AI is so vulnerable, you need to understand what Poyar calls “the curse of the AI wrapper.”

Most consumer AI apps are, at their core, thin layers built on top of foundation models from OpenAI, Anthropic, Google, or Meta. They add a user interface, some prompt engineering, maybe a specific use case focus — and then they charge $10 or $20 a month for the privilege. The problem is that the underlying models are improving at a pace that makes yesterday’s differentiation tomorrow’s commodity.

When GPT-3.5 was the best available model, a consumer app that used it cleverly for, say, writing assistance had genuine value. Then GPT-4 came out, and suddenly the base model could do most of what the wrapper was doing. Then GPT-4o. Then o1. Then o3. Each new model release is a potential extinction event for any consumer AI product that hasn’t built something genuinely proprietary on top of the model layer.

This is the fundamental structural problem with B2C AI investment: the moat is shallow, and it’s getting shallower every six months. The product that seemed defensible when you wrote the check may be commoditized by the time you’re hoping for a Series B.

B2B AI companies face this same technological risk, but they have something consumer apps don’t: deep integration into enterprise workflows. When an AI tool is embedded in a company’s ERP system, connected to its CRM, trained on its proprietary data, and used by 200 employees every day, ripping it out isn’t a matter of clicking “cancel subscription.” It’s a multi-month migration project with real organizational costs. That’s a moat. That’s what makes revenue durable.

The Structural Advantages of Enterprise AI

The differences between B2B and B2C AI aren’t just about churn rates. They run deeper, into the fundamental economics of how these businesses operate.

Longer Sales Cycles Create Stickier Customers

B2B AI sales cycles are notoriously long. A mid-market enterprise might take six to twelve months to evaluate, pilot, and deploy an AI solution. That’s frustrating for founders trying to grow quickly. But it’s actually a feature, not a bug, from an investor’s perspective.

The reason sales cycles are long is that enterprise buyers are doing real due diligence. They’re evaluating integration requirements, security posture, compliance implications, and ROI projections. By the time they sign a contract, they’ve made a genuine commitment. They’ve allocated budget. They’ve assigned internal champions. They’ve told their board they’re doing this.

Consumer AI users, by contrast, sign up in thirty seconds with a credit card. The same frictionlessness that makes consumer apps grow quickly makes them easy to abandon. There’s no organizational commitment, no sunk cost, no internal champion whose job depends on making the tool work.

Enterprise Contracts Provide Revenue Predictability

When a B2B AI company closes a deal, it typically closes an annual or multi-year contract. According to SaaS benchmarking data, multi-year contracts (lasting 2.5 years or more) show an 8.5% churn rate, compared to 16% for month-to-month agreements. Annual contracts also give companies more time to demonstrate value and build relationships before renewal conversations begin.

Consumer AI products almost universally operate on monthly subscriptions. This means every month is a renewal decision. Every month, the user is implicitly asking: “Is this worth $15?” And every month, a new competitor might be offering something shinier for $10.

For investors modeling cash flows and building DCF analyses, the difference between annual enterprise contracts and monthly consumer subscriptions is enormous. Annual contracts allow for more reliable revenue forecasting, more confident hiring plans, and more rational capital allocation. Monthly consumer subscriptions create a constant anxiety about next month’s numbers.

The ROI Conversation Changes Everything

Perhaps the most important structural advantage of B2B AI is that enterprise buyers think in terms of ROI. They’re not buying an AI tool because it’s cool or because their friends are using it. They’re buying it because they believe it will save money, generate revenue, or reduce risk. And because they’re thinking in ROI terms, they’re willing to pay prices that reflect genuine value creation.

Research from IT Pro across UK and European markets demonstrates that nearly two-thirds of B2B revenue leaders achieve positive return on investment within the first year of AI implementation. When customers are seeing positive ROI, they don’t cancel. They expand. They tell their colleagues. They become the internal champions who fight for budget increases at renewal time.

McKinsey research shows that B2B sales organizations implementing AI technologies achieve 13–15% revenue growth alongside 10–20% improvements in sales ROI. These are the kinds of numbers that make enterprise buyers want more, not less, of what they’re buying.

Consumer AI users, by contrast, are often buying on the basis of curiosity or convenience. When the curiosity fades — and it always does — there’s no ROI calculation keeping them subscribed.

The Data Moat: B2B AI’s Secret Weapon

There’s another dimension to B2B AI’s durability that doesn’t get enough attention: proprietary data.

When an enterprise deploys an AI tool, it typically feeds that tool with its own data — customer records, transaction histories, internal documents, product catalogs, support tickets. Over time, the AI model becomes trained on and optimized for that company’s specific context. The outputs become more accurate, more relevant, and more valuable precisely because they’re informed by data that no competitor can access.

This creates a compounding advantage. The longer a company uses a B2B AI tool, the more valuable that tool becomes — and the more painful it would be to switch to a competitor who would have to start from scratch with the company’s data. This is the data moat, and it’s one of the most powerful competitive advantages in enterprise software.

Consumer AI products have no equivalent. A user’s chat history with one AI assistant doesn’t transfer to another. Their preferences, their writing style, their frequently asked questions — none of it creates meaningful switching costs. The consumer can move to a competitor in minutes, taking nothing of value with them.

As noted by Flippa’s analysis of AI startup valuations, AI companies that build strong intellectual property moats through proprietary algorithms and data networks create compounding competitive advantages. Unlike traditional software, where switching costs may be lower, AI models improve with data accumulation. This dynamic is far more pronounced in B2B contexts, where enterprise data is both more voluminous and more proprietary.

The Numbers Behind B2B AI Adoption

The adoption story for B2B AI is also considerably more robust than the consumer narrative suggests.

According to research compiled by SerpSculpt, 67% of B2B e-commerce firms have deployed AI and machine learning technologies to accelerate business growth, while 78% of all B2B companies utilize AI across at least one business function. Critically, 41% of B2B e-commerce firms have achieved full AI integration across operations — not just pilots, not just experiments, but production deployments embedded in core workflows.

Perhaps most telling for investors: 66% of B2B companies plan to increase AI investment over the next 24 months, and 90% classify AI as critical to their long-term strategic objectives. These aren’t companies that are going to cancel their AI subscriptions next quarter. These are companies that are building their competitive strategies around AI and will need more of it, not less.

The Stanford HAI 2025 AI Index Report confirms the macro picture: U.S. private AI investment grew to $109.1 billion in 2024, with generative AI attracting $33.9 billion globally — an 18.7% increase from 2023. The money is flowing, and a disproportionate share of it is flowing into enterprise applications.

Dentsu estimates that 77% of all B2B buying processes used AI in 2025, and that the proportion of heavy users grew to 40%. Forrester reports that 89% of B2B buyers have adopted generative AI as one of the top sources of self-guided information throughout every phase of their buying process. These aren’t vanity metrics — they’re indicators of deep, structural integration that creates durable demand.

The Valuation Picture: Premium Multiples for Durable Revenue

The financial markets have noticed what the retention data is telling us. B2B AI companies with strong enterprise contracts and high NRR are commanding premium valuations — and those valuations are more defensible than the headline numbers for consumer AI darlings.

According to Aventis Advisors’ analysis of AI valuation multiples, the median revenue multiple for AI companies stood at approximately 29.7x in 2025, with fundraising rounds pricing around 25–30x EV/Revenue at the median. But these numbers mask enormous variation based on the quality and durability of the underlying revenue.

Flippa’s analysis breaks down the range: early-stage AI startups command 10x–50x revenue multiples, growth-stage companies 8x–20x, and mature AI startups 5x–12x. Within these ranges, the companies commanding the highest multiples are consistently those with enterprise contracts, high NRR, and deep workflow integration — the hallmarks of B2B AI.

The reason is straightforward: valuation is ultimately a function of the present value of future cash flows. When you have high NRR, your future cash flows are more predictable and more likely to grow. When you have low NRR — as most consumer AI products do — your future cash flows are uncertain and potentially declining. The market prices this difference, and it prices it significantly.

As Equidam’s analysis of AI startup valuations points out, a company with $10M ARR and $15M in compute costs looks identical to one with $10M ARR and $2M in compute costs when you’re applying a revenue multiple. But their fundamental value is completely different. The same logic applies to retention: a company with $10M ARR and 85% NRR is worth dramatically more than one with $10M ARR and 48% NRR, even if the headline revenue number looks the same.

The “AI Achiever” Gap

One of the most revealing data points in the B2B vs. B2C AI debate comes from a Lucidworks study that used an agentic AI tool to assess more than 1,100 companies — evaluating actual AI deployments rather than relying on self-reported claims.

The study found that 41% of B2C companies qualified as “achievers” — organizations deploying both core and advanced AI capabilities that measurably improve customer experiences. For B2B companies, the number was 31%. On the surface, this looks like a point in favor of B2C AI. B2C companies are adopting AI faster, right?

But look more carefully at what this data actually means for investors. The fact that B2B companies are adopting AI more slowly and more deliberately is a feature, not a bug. Enterprise AI adoption is methodical because the stakes are higher and the integration requirements are more complex. When a B2B company finally deploys an AI solution at scale, it’s because they’ve done the due diligence, secured the budget, and committed to the technology. That’s durable adoption.

B2C AI adoption, by contrast, can be fast precisely because it’s shallow. Downloading an app and paying $10 a month is easy. It’s also easy to cancel. The speed of B2C adoption is inversely correlated with its durability.

Michael Sinoway, CEO of Lucidworks, put it well in commenting on the study: “Cost unfortunately seems to have been a too predominant evaluation factor… you end up having lower quality. Success comes from applying AI where it creates genuine value, not everywhere at once.” This is the B2B AI thesis in a sentence.

The Competitive Dynamics: Why B2C AI Is a Race to the Bottom

There’s a competitive dynamic in consumer AI that should terrify investors: the market is structurally designed to commoditize.

Consumer AI products compete primarily on capability and price. Capability is determined largely by the underlying foundation model, which is controlled by a handful of companies — OpenAI, Anthropic, Google, Meta — who are in a relentless arms race to improve their models. Price is determined by competition, which is fierce and getting fiercer.

The result is a market where the best consumer AI products are constantly being undercut by better foundation models that make their differentiation obsolete, and where price competition is driving margins toward zero. This is not a market structure that produces durable investor returns.

B2B AI markets have a very different competitive dynamic. Enterprise buyers don’t switch vendors primarily on the basis of which underlying model is slightly better. They switch — or don’t switch — based on integration depth, customer success quality, compliance certifications, and the organizational cost of migration. These are factors that take years to build and can’t be replicated overnight by a competitor with a better model.

The result is a market where competitive advantages are durable, where pricing power is real, and where the best companies can build genuine moats. This is a market structure that produces investor returns.

The Palantir Playbook: Services as a Moat

One of the most instructive examples of how B2B AI companies build durable competitive advantages comes from Palantir, which has famously deployed what it calls “forward-deployed engineers” (FDEs) — technical staff who embed with enterprise clients to prototype and implement AI solutions.

As noted in the ChartMogul/Poyar analysis, many AI companies, including OpenAI, are following Palantir’s lead. The FDE model trades margin for moat — it’s expensive to deploy engineers to client sites, but it creates an integration depth that makes the product nearly impossible to rip out. The client’s workflows, data pipelines, and institutional knowledge become intertwined with the vendor’s technology.

This is a strategy that simply doesn’t exist in consumer AI. You can’t deploy forward-deployed engineers to help individual users get more value from a $15/month writing assistant. The economics don’t work, and the use case doesn’t warrant it. But in enterprise AI, where a single contract might be worth $500,000 or $5 million per year, the FDE model is not just viable — it’s a powerful competitive weapon.

The broader lesson is that B2B AI companies have access to a range of moat-building strategies — deep integration, proprietary data, customer success programs, compliance certifications, multi-year contracts — that simply aren’t available to consumer AI products. This asymmetry in moat-building potential is one of the most important reasons B2B AI investors sleep better.

The Agentic AI Wave: B2B’s Next Advantage

The next major wave of AI development — agentic AI, systems that autonomously plan, execute, and complete multi-step tasks with minimal human oversight — is poised to deepen B2B AI’s structural advantages even further.

According to Gartner projections cited by Commercetools, 90% of B2B buying will be AI agent-intermediated, pushing over $15 trillion in B2B spend through AI agent exchanges by 2028. The emergence of autonomous purchasing agents, AI-powered sales agents, and intelligent post-purchase agents will create new layers of integration between enterprise AI tools and business workflows.

Each layer of integration is another layer of switching cost. Each autonomous agent that becomes embedded in a company’s procurement process, sales pipeline, or customer success workflow is another reason not to switch vendors. The agentic AI wave isn’t just a product opportunity for B2B AI companies — it’s a moat-deepening opportunity.

Consumer AI is also developing agentic capabilities, but the dynamics are different. Consumer agents help individuals with tasks like scheduling, research, and shopping. These are valuable, but they don’t create the same organizational lock-in as enterprise agents embedded in business-critical workflows. A consumer can switch from one AI agent to another relatively easily. An enterprise that has built its procurement process around an AI agent cannot.

The Gross Margin Problem: A Hidden Risk in Consumer AI

There’s another dimension to the B2C AI investment risk that doesn’t get enough attention: gross margins.

Consumer AI products face a structural gross margin challenge that B2B AI companies can often avoid. Every inference — every time a user asks the AI a question or generates content — costs money. These compute costs are real and significant, and they scale with usage. For a consumer product charging $10 or $15 per month, the economics can be brutal: a heavy user might generate more in compute costs than they pay in subscription fees.

B2B AI companies can address this problem in ways that consumer products cannot. Enterprise contracts can be structured to include usage-based pricing that ensures compute costs are covered. Enterprise customers can be educated about efficient usage patterns. And enterprise use cases often involve more structured, predictable workloads that are easier to optimize for cost efficiency.

As Equidam’s analysis notes, OpenAI’s situation — spending over $5 billion on compute against $4.9 billion in revenue — illustrates the fundamental challenge of building a sustainable AI business when compute costs are not properly managed. This challenge is most acute in consumer AI, where price sensitivity limits the ability to charge prices that reflect true cost.

What the Smart Money Is Doing

The sophisticated investors who have been in enterprise software for decades understand these dynamics intuitively. They’ve seen the SaaS playbook play out — the early excitement, the churn problems, the eventual realization that B2B SaaS with high NRR is one of the best business models ever invented. They’re applying the same lens to AI.

Crunchbase data cited by the Stanford HAI report shows that total AI investment hit $95 billion in 2024, a new record. But look at where the money is going: infrastructure, enterprise applications, vertical SaaS with AI capabilities. The mega-rounds — the $1 billion+ deals — are going to companies with enterprise revenue, not consumer apps.

The venture firms that have been most consistently successful in AI — Andreessen Horowitz, Sequoia, Bessemer — have all made significant bets on enterprise AI. They’re not ignoring consumer AI entirely, but their highest-conviction positions are in companies with enterprise contracts, high NRR, and deep workflow integration.

This isn’t a coincidence. It’s the result of pattern recognition from decades of investing in software. The patterns that produce durable returns in software — sticky customers, expanding revenue, high gross margins, defensible competitive positions — are all more reliably present in B2B AI than in B2C AI.

The Counterargument: Why B2C AI Still Attracts Capital

To be fair, there are legitimate reasons why investors continue to fund consumer AI companies, and it’s worth engaging with those arguments honestly.

The first is scale. Consumer AI products can reach millions of users in ways that enterprise products cannot. A viral consumer AI app can go from zero to a million users in weeks. No enterprise product has ever done that. For investors who believe that scale creates its own moat — through data network effects, brand recognition, or platform dynamics — consumer AI can be attractive.

The second is optionality. Some consumer AI products are building toward something more durable — a platform, a data asset, a brand — that could eventually support enterprise revenue. The consumer product is a customer acquisition channel for a future enterprise business. This is a legitimate strategy, though it requires investors to be patient and to believe in the pivot.

The third is the possibility of genuine consumer lock-in. A small number of consumer AI products are building real switching costs — through personalization, through integration with personal data, through habit formation. If a consumer AI product becomes genuinely indispensable to a user’s daily life, the churn dynamics can improve dramatically. But these products are rare, and identifying them in advance is extremely difficult.

The honest assessment is that these counterarguments apply to a small minority of consumer AI companies. For most consumer AI products — the AI writing assistants, the AI image generators, the AI chatbots — the structural challenges of churn, commoditization, and margin compression are real and severe.

The Path Forward: What B2B AI Investors Should Watch

For investors who are already in B2B AI, or who are considering entering the space, there are several key metrics and dynamics worth monitoring.

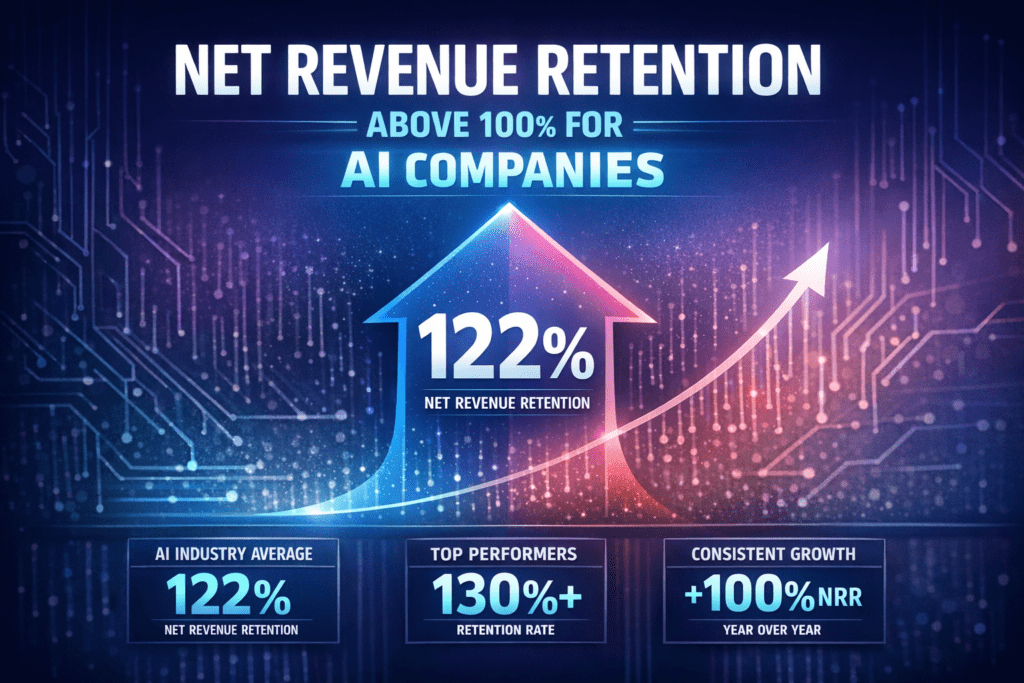

Net Revenue Retention above 100% is the gold standard. It means existing customers are expanding their usage faster than any customers are churning. According to ChartMogul’s SaaS Benchmarks Report, a high NRR often correlates with better growth, efficiency, and higher valuations. B2B AI companies with NRR above 110% are in elite territory.

Workflow integration depth matters more than feature count. The question isn’t how many things an AI product can do — it’s how deeply embedded it is in the customer’s core workflows. A product that touches one workflow is vulnerable; a product that touches ten is nearly impossible to displace.

Proprietary data accumulation is a leading indicator of long-term defensibility. B2B AI companies that are building proprietary datasets — through customer data, through usage patterns, through domain-specific training — are building moats that will compound over time.

Enterprise contract structure — annual vs. monthly, multi-year vs. single-year — is a direct predictor of retention. SaaS benchmarking data consistently shows that multi-year contracts have dramatically lower churn than month-to-month agreements. B2B AI companies that can move customers to multi-year contracts are building more durable revenue bases.

Vertical specialization is increasingly important. As Flippa’s analysis notes, investors are prioritizing AI startups that solve real-world business problems in specific industries rather than those developing general-purpose models. Vertical AI companies — those focused on healthcare, legal, financial services, manufacturing — can build domain expertise and compliance certifications that create genuine barriers to entry.

The Verdict: Sleep Quality as an Investment Thesis

The title of this article is a bit tongue-in-cheek, but the underlying point is serious. Investment quality is ultimately about risk-adjusted returns — about how much uncertainty you’re taking on relative to the returns you expect to generate.

B2B AI investors are taking on real risks. Enterprise sales cycles are long and unpredictable. Integration projects can fail. Competition from large platform vendors — Microsoft, Salesforce, Google — is real and intensifying. The technology is evolving rapidly, and today’s differentiated product can become tomorrow’s commodity.

But these risks are manageable. They’re the kinds of risks that experienced enterprise software investors know how to evaluate and mitigate. They’re risks that can be addressed through product strategy, customer success investment, and competitive positioning.

B2C AI investors are taking on a different kind of risk — one that is harder to manage because it’s more structural. When your product’s core differentiation is a thin layer on top of a foundation model that is improving every six months, you’re not just competing with other startups. You’re competing with the foundation model providers themselves, who have every incentive to absorb your use case into their base product. That’s a race you can’t win.

The ChartMogul data makes the stakes clear: AI-native companies with median GRR of 40% are burning through their total addressable market. Companies that make it to $5 million ARR have substantially better retention than their early-stage peers — but getting there requires surviving the churn wave, which most won’t.

B2B AI companies, by contrast, are building the kind of durable, compounding businesses that generate the returns investors actually need. They’re building on the same foundation — large language models, generative AI, agentic systems — but they’re building on top of it in ways that create genuine value for customers, genuine switching costs, and genuine competitive moats.

That’s why B2B AI investors are sleeping better. Not because they’ve found a risk-free investment — there’s no such thing. But because they’ve found a category where the risks are manageable, the moats are real, and the business fundamentals actually work.

In the AI era, as in every era of technology investment, the companies that win are the ones that solve real problems for customers who have real budgets and real reasons to stay. That description fits B2B AI far better than it fits B2C AI. And that’s a thesis worth betting on.

Kingy Launch Brief

Put the week’s verified AI launches in your inbox.

The public Friday pilot has not sent its first issue yet. Join for a source-checked launch briefing with a clear try, watch or skip verdict, then check your inbox and confirm your address.

Free · Friday pilot · Double opt-in · Unsubscribe anytime