The AI revolution isn’t one wave. It’s four — and they’re all hitting at once.

In early 2026, Elon Musk reached for a metaphor that was both dramatic and precise. The current technological moment, he said, was not a gentle wave of change. It was a “Supersonic Tsunami.” The phrase has since taken on a life of its own in boardrooms, venture capital pitches, and government briefings — because it captures something that conventional language struggles to convey.

This is not a single innovation cycle, like the dawn of the internet or the mobile revolution. It is a convergence of multiple, simultaneous tsunamis — in artificial intelligence, physical infrastructure, energy, and computing hardware — each amplifying the others, creating a compounding force of unprecedented scale.

As technologist and XPRIZE founder Peter H. Diamandis has noted, we are witnessing a fundamental phase shift. AI is no longer improving linearly. Instead, three exponential curves are hitting their inflection points simultaneously: the raw power of computational hardware, the sophistication of AI models, and the physical deployment of the systems that run them. When exponentials converge, the result isn’t incremental progress. It’s a sudden, systemic disruption that rewrites the rules of business, economics, and society itself.

The evidence is no longer theoretical. It’s visible in financial reports that defy historical precedent, in capital expenditure commitments that rival the GDP of small nations, and in scientific breakthroughs that are collapsing decades-long research timelines into mere months. We are moving from an economy of scarcity — where progress was constrained by the high cost of intelligence, energy, and labor — to what Diamandis calls an “Abundance Economy,” where these fundamental inputs are becoming radically cheaper and more accessible.

This article is a comprehensive analysis of that supersonic tsunami. We will dissect the four primary mega-trends driving this transformation: the explosive growth in AI revenue, the historic build-out of physical infrastructure, the race to solve the corresponding energy equation, and the revolution in semiconductor technology.

We will explore how these forces are not separate but are part of one interlocking, self-reinforcing system. And we will provide actionable insights for entrepreneurs, investors, executives, and students on how to navigate this new world — how to build on the crest of the wave rather than being buried by it.

The future isn’t ten years away. It is being deployed now.

Part One: The AI Revenue Explosion

The abstract promise of artificial intelligence has finally materialized into a concrete, staggering financial reality. The revenue growth currently being posted by leading AI companies is not just impressive — it is unprecedented in the history of business, dwarfing the ascent of previous software-as-a-service darlings like Slack, Zoom, or Snowflake. This financial explosion is the clearest indicator that AI has crossed a critical threshold, moving from a niche technology to a fundamental economic engine.

The New Benchmarks of Growth

Consider Anthropic, a company focused on developing safe and steerable AI. In December 2024, it reached an annualized revenue run rate (ARR) of $1 billion. Just 14 months later, by February 2026, that figure had skyrocketed to $14 billion. By March 2026, the company was already approaching a $20 billion run rate, having more than doubled from its $9 billion ARR at the end of 2025.

To put this in perspective, Anthropic’s monthly revenue of roughly $1.6 billion now exceeds what a high-growth company like Snowflake generates in an entire quarter. This represents a sustained 10x year-over-year growth rate — a pace with no parallel in the B2B software sector.

Its primary competitor, OpenAI, is scaling at a similarly breathtaking velocity. After booking $13.1 billion in full-year revenue for 2025, the company reached a $25 billion ARR by the end of February 2026. Projections for the coming years are even more audacious, with internal targets aiming for $85 billion by 2030 and some analyst models forecasting $100 billion in recurring revenue as early as 2027.

Crucially, this revenue is not coming from consumer novelty. Anthropic’s growth is overwhelmingly enterprise-driven: approximately 80% of its revenue comes from businesses, with 70–75% generated through pay-per-token API calls from enterprises and developers. The depth of enterprise penetration is remarkable. The number of customers spending over $100,000 annually has increased sevenfold in the past year. Over 500 companies now spend more than $1 million annually on Claude products — a staggering rise from just a dozen two years prior. Eight of the Fortune 10 companies are now Claude customers.

This meteoric rise has been matched by soaring valuations. In February 2026, Anthropic closed a monumental $30 billion Series G funding round, catapulting its post-money valuation to $380 billion. The round was led by a consortium of global giants including Singapore’s GIC, Coatue, and Founders Fund, with capital from Microsoft and NVIDIA.

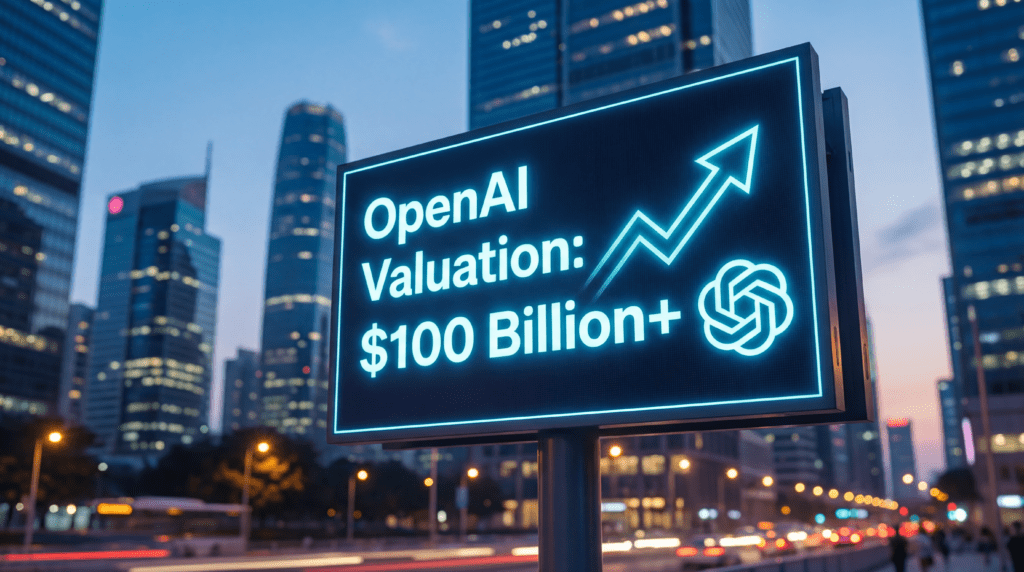

Meanwhile, OpenAI’s valuation has entered the stratosphere. A secondary share sale in late 2025 valued the company at $500 billion, but by February 2026, a new investment round — including $30 billion from Nvidia and $50 billion from Amazon — was announced at a pre-money valuation of $730 billion. The company is now laying the groundwork for what could be the largest IPO in history, with a potential target valuation of up to $1 trillion.

Yet these staggering valuations also reflect the immense capital required to compete at the frontier. Despite its explosive revenue, OpenAI is burning cash at a prodigious rate — a projected $8.5 billion in 2025 and $17 billion in 2026 — driven by the enormous cost of training cutting-edge models and building infrastructure.

The company’s compute obligations are estimated at $450 to $650 billion between 2024 and 2030, and it is not expected to be free-cash-flow positive until the end of the decade. This underscores a crucial dynamic of the AI economy: the scale of capital required to compete at the frontier is so vast that only a handful of players can afford to stay in the race, creating a natural oligopoly at the top.

The conviction behind these numbers is perhaps best illustrated by the actions of NVIDIA CEO Jensen Huang, who has more visibility into the AI infrastructure pipeline than anyone on Earth. In early 2026, he finalized a $30 billion investment in OpenAI and a $10 billion investment in Anthropic — telling investors these would likely be NVIDIA’s last private investments in the companies before they enter public markets. This $40 billion pre-IPO bet from the market’s most informed player is a powerful signal that the growth is not speculative. It’s real, and it’s just getting started.

The Paradigm Shift: From IT Budgets to Labor Budgets

What is fueling this unprecedented financial engine? The answer marks a fundamental change in the economic role of technology. For decades, enterprise software competed for a slice of a company’s Information Technology budget. AI has broken out of this confinement. The latest generation of models have crossed a crucial capability threshold where they are no longer just tools to make existing processes more efficient. They are now powerful enough to augment and, in some cases, automate human labor itself.

Companies are no longer buying AI to replace servers. They are buying it to supplement and displace human cognitive work. The spending is shifting from the CIO’s IT budget to the COO’s and CEO’s much larger labor budget. As TechCrunch reported, investors increasingly predict that “agentic AI” systems — autonomous agents capable of performing complex tasks — will capture value from the vast global pool of labor costs, a market orders of magnitude larger than the entire software industry.

This shift is already underway. Surveys show that companies are reallocating funds from other areas to finance AI adoption, delaying non-critical infrastructure upgrades and consolidating traditional software licenses to free up capital for AI platforms and API calls. Some firms are reducing their reliance on human contractors for tasks like data analysis and redirecting those funds to AI software that can empower their remaining internal staff.

While the narrative of AI-driven job displacement is complex, the economic calculus for businesses is becoming brutally simple: if intelligence can be purchased as a utility, on a metered, pay-per-token basis, it represents a powerful new lever for productivity and cost management.

Case Study: The Coding Revolution

Nowhere is this shift from labor to AI more apparent than in the world of software development. For decades, the primary rate-limiting factor for nearly every technology company has been the availability of skilled software engineers. The demand has always outstripped supply, with top talent flowing to a handful of elite firms in Silicon Valley.

AI coding assistants have shattered this constraint. Tools like Anthropic’s Claude Code and GitHub Copilot are not just helping developers write code faster — they are becoming active partners in the creative process, capable of tackling complex, multi-file projects autonomously.

The financial impact has been immediate and explosive. Claude Code, launched in May 2025, went from zero to an annualized revenue run rate of over $2.5 billion in just nine months. Its revenue run rate more than doubled in the first two months of 2026 alone, with enterprise use now accounting for over half of that total. The tool’s VS Code extension installs surged from 17.7 million to 29 million since the start of 2026, and it is projected to be responsible for over 20% of all daily commits on GitHub by the end of the year.

GitHub Copilot, the market incumbent, has also seen massive adoption, crossing 20 million all-time users by mid-2025, with 90% of Fortune 100 companies utilizing the tool. Enterprise teams using Claude Code have reported a 4:1 ROI, calculating that the cost per incremental pull request is just $37.50, compared to $150 in saved developer time.

This is the “supersonic tsunami” in its financial form: exponential capability leading to exponential adoption, which in turn fuels an exponential explosion in revenue. It is a cycle that is not just creating wealth for a few AI labs but is fundamentally re-architecting the cost structure of modern business.

Part Two: The Infrastructure Buildout

The staggering revenue figures and multi-trillion-dollar market forecasts for AI are not built on abstract algorithms alone. They are being forged in steel, concrete, and silicon. We are in the midst of the largest and fastest infrastructure build-out in the history of technology — a global construction project that dwarfs previous cycles like the rollout of fiber optics or 4G networks. This physical manifestation of the AI revolution is where the digital world of models and data meets the terrestrial world of capital, energy, and logistics.

The $690 Billion Hyperscaler Spree

At the epicenter of this build-out are the world’s largest technology companies — the “hyperscalers.” The five dominant U.S. players — Microsoft, Alphabet (Google), Amazon, Meta, and Oracle — are collectively projected to spend a jaw-dropping $690 billion on capital expenditures in 2026 alone. This figure represents a near-doubling of their 2025 spending levels and signals an all-in commitment to winning the AI arms race.

The vast majority of this capital — estimated at around 75%, or over $450 billion — is being funneled directly into AI-specific infrastructure: state-of-the-art data centers, millions of specialized GPUs, high-speed networking fabric, and advanced cooling systems. This spending is so aggressive that it is fundamentally altering the financial profiles of these companies. Their capital intensity — capex as a percentage of revenue — has soared to between 45–57%, a level more commonly associated with heavy industrial or utility companies than with software firms.

The individual commitments for 2026 are monumental:

- Amazon: A projected $200 billion in capex, with the lion’s share dedicated to AWS and its AI capabilities.

- Alphabet (Google): An expected spend of between $175 billion and $185 billion to expand its cloud and AI footprint.

- Microsoft: On track for $120 billion or more as it builds out the infrastructure to support its Azure cloud and its deep partnership with OpenAI.

- Meta: A planned investment of $115 billion to $135 billion, pivoting its massive infrastructure towards AI research and product integration.

- Oracle: A targeted $50 billion — a 136% increase from 2025 — driven by massive contracts to provide cloud infrastructure for AI leaders like OpenAI.

This spending spree is so intense that it is projected to consume nearly all of some companies’ free cash flow. Alphabet’s free cash flow, for example, is forecast to plummet almost 90% — from over $73 billion in 2025 to just $8.2 billion in 2026 — as capital expenditures absorb virtually every dollar generated. To bridge the gap, hyperscalers are increasingly turning to debt markets on a massive scale, collectively raising $108 billion in debt in 2025 alone.

Building the AI Factories

According to market research firm Gartner, total worldwide AI spending is forecast to hit $2.53 trillion in 2026, a 44% increase over 2025. A huge portion of this is dedicated to foundational hardware — Gartner projects that spending on AI infrastructure specifically will reach $1.37 trillion in 2026.

NVIDIA CEO Jensen Huang has offered an even grander vision. He estimates that the world will need to spend between $3 trillion and $4 trillion by the end of the decade to completely overhaul its existing computing infrastructure for the age of AI. This isn’t about adding a few more servers. It’s about building an entirely new economic substrate — the “electricity grid of the 21st century.”

This investment is manifesting in a global data center construction boom of historic proportions. The United States is the epicenter, with an estimated $77.7 billion in data center construction starts in 2025 alone, concentrated in states with available land and power like Texas, Louisiana, and Virginia. The cost of construction is also rising sharply: the global average cost to build a data center climbed from $7.7 million per megawatt in 2020 to $10.7 million per megawatt in 2025.

These are not the data centers of the past. They are “AI factories” — gigawatt-scale facilities designed for the sole purpose of training and running massive AI models. A new rule of thumb has emerged in the industry: it costs approximately $50 billion to build one gigawatt of AI data center capacity.

The potential return justifies the colossal upfront investment — the same industry rule of thumb suggests that a one-gigawatt facility can generate approximately $10 billion in annual revenue. When you are spending $50 billion on a single facility and generating $10 billion a year from it, you are not just building a product. You are creating a new form of high-yield infrastructure.

The NVIDIA Choke Point

At the heart of every AI factory is the GPU, and at the heart of the GPU market is NVIDIA. The company commands an astonishing 80–90% of the AI accelerator market, with its share of the discrete GPU market hitting 92% in the first half of 2025. This dominance is cemented by its CUDA software platform, which has become the ubiquitous programming environment for AI development.

However, the industry’s ability to spend the trillions of dollars being allocated is hitting a hard wall of physical constraints. The AI supply chain is stretched to its breaking point, with critical bottlenecks expected to persist well into 2026 and beyond:

- Advanced Packaging (CoWoS): NVIDIA relies on TSMC’s “Chip-on-Wafer-on-Substrate” technology to connect GPU silicon with high-bandwidth memory. TSMC’s entire CoWoS capacity is fully booked through 2026, with demand far outstripping its ability to expand.

- High-Bandwidth Memory (HBM): The specialized HBM3 and HBM3E memory chips crucial for AI accelerators are also sold out through 2026, with costs expected to rise 15–20%.

- Leading-Edge Wafers: Demand for the most advanced 3nm and 2nm semiconductor wafers from foundries like TSMC is reportedly three times greater than the available supply.

These structural bottlenecks mean that even with unlimited capital, the pace of the AI infrastructure build-out is ultimately governed by the global manufacturing capacity for a few highly specialized components. This is the physical reality of the supersonic tsunami: a wave of capital so immense it is crashing against the absolute limits of our industrial capacity.

Part Three: The Energy Equation

The AI infrastructure build-out has an insatiable appetite. Its fuel is electricity, and its consumption is growing at a rate that is beginning to challenge the capacity of our global energy systems. The elephant in the room for the AI revolution is the energy equation: can we generate and deliver enough clean power to sustain this exponential growth?

The scale of the problem is daunting. Global electricity demand from data centers is on track to more than double by 2030, reaching around 945 terawatt-hours — an amount roughly equivalent to the entire annual electricity consumption of Japan. AI is the primary driver of this surge. In the United States alone, data centers are projected to account for nearly half of all electricity demand growth between now and 2030.

A 2024 report from Lawrence Berkeley National Laboratory paints an even starker picture. It projects that U.S. data center electricity demand will grow from 176 TWh in 2023 to between 325 and 580 TWh by 2028. At the high end, this would represent 12% of total U.S. electricity consumption, up from just 4.4% in 2023. The grid was simply not designed for this kind of concentrated, rapid load growth. In high-demand regions like Northern Virginia, data centers already consume over a quarter of the total electricity supply.

This energy bottleneck threatens to become the single greatest constraint on the future of AI. Yet, in a perfect illustration of the converging tsunami, the scale of the problem is catalyzing an equally scaled response.

The Fusion Race Heats Up

For decades, nuclear fusion — the process that powers the sun — has been the ultimate dream of clean energy, perpetually “30 years away.” That timeline is collapsing in real time.

The private sector is moving at an unprecedented pace. Total investment in private fusion companies has surged five-fold since 2021, reaching nearly $10.6 billion across 53 companies by 2025. Eighty-four percent of fusion companies surveyed believe they will deliver fusion-generated electricity to the grid before the end of the 2030s.

Two companies are leading the charge:

Commonwealth Fusion Systems (CFS), a spin-off from MIT, has raised nearly $3 billion from investors including NVIDIA and Google. Its strategy revolves around using powerful high-temperature superconducting magnets to create a compact, commercially viable tokamak reactor. Its demonstration machine, SPARC, is currently being assembled and is expected to achieve “first plasma” in late 2026. The crucial milestone — producing more energy than it consumes — is targeted for early 2027. This paves the way for ARC, its first grid-connected, 400-megawatt power plant, slated for the early 2030s.

Helion Energy, backed by OpenAI CEO Sam Altman, takes a different approach using pulsed magnetic compression rather than a traditional tokamak. The company has a history of rapid iteration, having built and tested seven fusion prototypes. Its sixth prototype, Trenta, became the first private fusion device to reach 100 million degrees Celsius — the minimum threshold for commercial viability. Helion has already begun construction of its first commercial fusion plant, Orion, in Washington state. In a landmark deal — the world’s first commercial agreement for fusion energy — Helion will supply power directly to Microsoft’s data centers starting in 2028. The plant is designed to generate at least 50 megawatts of electricity, demonstrating a direct line from fusion research to powering the AI boom.

Simultaneously, government-backed projects are shattering long-held records. In early 2025, China’s “Artificial Sun” EAST reactor sustained a high-confinement plasma for nearly 18 minutes — a world record for duration. Shortly after, France’s WEST tokamak surpassed this, maintaining a stable plasma for over 22 minutes. More profoundly, researchers at EAST demonstrated stable operation at plasma densities 30–65% above the theoretical “Greenwald limit,” a barrier long considered a fundamental constraint on fusion reactor performance.

Ironically, the technology creating the power problem is also helping to solve it. DeepMind, Google’s AI lab, has developed a deep reinforcement learning system that can autonomously control the complex magnetic fields inside a tokamak, stabilizing the plasma with superhuman precision. This AI controller has already been used to sculpt the plasma into novel, highly efficient shapes that were previously impossible to maintain, dramatically speeding up the experimental cycle. DeepMind is now collaborating directly with CFS, using its AI models to optimize the design and operation of the SPARC reactor — increasing the probability of achieving net energy on an accelerated timeline.

The Nuclear Revival

While fusion represents the long-term future, the immediate need for massive, 24/7 carbon-free power has triggered a renaissance for a more established technology: nuclear fission. After decades of stagnation in the West, tech giants are now directly investing in restarting and building nuclear power plants to energize their AI factories.

In a groundbreaking move, Microsoft signed a 20-year, $16 billion power purchase agreement with Constellation Energy to restart Unit 1 of the Three Mile Island nuclear power plant in Pennsylvania. The reactor, which was shut down in 2019, is set to come back online in 2028, providing 835 megawatts of dedicated, carbon-free baseload power for Microsoft’s growing network of AI data centers.

Amazon Web Services has made a similar commitment. It acquired a data center campus directly adjacent to Talen Energy’s 1.92 GW Susquehanna nuclear plant in Pennsylvania and signed a 17-year power purchase agreement for the plant’s output. Amazon plans to invest over $20 billion to convert the site into an AI-ready campus powered entirely by carbon-free nuclear energy. Other tech giants have followed suit: Meta has announced a 20-year agreement to purchase 1.1 GW of nuclear energy from the Clinton Clean Energy Center in Illinois, while Oracle is planning a gigawatt-scale data center powered by three small modular reactors.

These deals signal a strategic shift. Tech companies are no longer passive consumers of electricity. They are becoming anchor tenants and financial backers for large-scale energy infrastructure — recognizing that intermittent renewables like solar and wind, while crucial, cannot alone provide the constant, unwavering power that AI data centers demand.

Part Four: The Chip Revolution

The energy solutions detailed above address the power supply problem from the outside — generating more electricity to feed into the grid. But the chip revolution attacks the same problem from the inside, by radically reducing how much power AI needs in the first place. The conventional computer chip architecture that has driven progress for the last 70 years is hitting its physical limits, unable to keep pace with the exponential demands of artificial intelligence. This has ignited a three-front war for the future of computing.

The Efficiency Imperative: Neuromorphic Computing

The most profound shift is happening at the level of chip design itself. Neuromorphic computing — a field that builds processors inspired by the architecture of the human brain — is moving from the research lab to commercial reality, promising to slash the energy consumption of AI tasks by orders of magnitude.

Traditional chips, based on the von Neumann architecture, waste enormous amounts of energy — up to 80% — simply shuttling data between separate processing and memory units. Neuromorphic chips overcome this “von Neumann bottleneck” by mimicking the brain’s structure, where processing and memory are co-located. They operate on two key principles: event-driven processing, where circuits only activate when new data arrives, and in-memory computing, which minimizes data movement — the single biggest source of energy waste in conventional AI accelerators.

The results are staggering. For certain AI inference tasks, neuromorphic systems have demonstrated energy efficiency improvements of 100 to 1,000 times over traditional GPUs. This is not a 10% improvement. It is a phase shift in the economics of computation.

Key players are already deploying this technology at scale. Intel’s Loihi 2 research chip powers the Hala Point system at Sandia National Laboratories — the world’s largest neuromorphic system, containing 1.15 billion artificial neurons, being used to tackle complex physics simulations at a fraction of the energy cost of a traditional supercomputer. IBM’s NorthPole chip, which entered production in 2026, is 25 times more energy-efficient than a high-end NVIDIA GPU for image recognition tasks and requires no complex liquid cooling.

When compute becomes this cheap and efficient, you don’t just do the same things faster. You do entirely new things that were previously economically impossible. Real-time protein folding for personalized medicine, complex drug discovery simulations running on desktop-scale hardware, and truly autonomous robots with long battery life all become viable.

Tesla’s Terafab: A Gamble on Vertical Integration

As the value of custom, high-performance silicon skyrockets, some companies are making the audacious move to take control of not just design, but manufacturing. On March 14, 2026, Elon Musk announced the formal launch of the “Terafab Project” — Tesla’s plan to build its own massive semiconductor fabrication plant.

This is a high-stakes gamble on vertical integration, estimated to cost between $20 and $25 billion. The goal is to produce between 100 and 200 billion custom AI and memory chips per year, using a cutting-edge 2-nanometer process. The ambition is to eventually scale to a capacity of one million wafer starts per month — a volume that would represent roughly 70% of the total output of the current industry leader, TSMC, all concentrated in a single U.S. facility.

The first chip slated for production at Terafab is Tesla’s fifth-generation AI chip, AI5. After discontinuing its specialized Dojo training supercomputer, Tesla has focused on a unified chip optimized for inference — the real-time execution of AI models inside its cars and Optimus humanoid robots. The AI5 is designed to deliver performance comparable to an NVIDIA H100 GPU at a fraction of the power, a critical requirement for vehicle and robot autonomy.

While the March 21 launch date marks a groundbreaking rather than a fully operational fab — a project of this scale takes years to build — the signal is monumental. Tesla is joining Apple, Google, and Amazon in the quest for custom silicon. But by attempting to also control manufacturing, a field of staggering complexity in which it has no experience, Tesla is making a bet that could either secure its technological dominance for a decade or become a colossal failure.

The Great Decoupling: China’s Push for Sovereignty

This dependence on a single company — TSMC — located in a geopolitically sensitive region, has not gone unnoticed. In response to tightening U.S. export controls that have cut off its access to top-tier NVIDIA chips, China has launched a massive national effort to build a self-reliant semiconductor industry.

Chinese tech giants are rapidly developing domestic alternatives to NVIDIA’s hardware and software. Huawei, through its HiSilicon division, is positioning its Ascend series of AI chips as a direct competitor, while also building a full software ecosystem — including its CANN platform — as a replacement for NVIDIA’s dominant CUDA. Cambricon is developing its Siyuan series with the goal of matching the performance of top-tier NVIDIA GPUs, supplying them to other Chinese giants like Baidu and Alibaba. And AI firm DeepSeek is optimizing its advanced large language models, like the upcoming trillion-parameter DeepSeek V4, to run specifically on Huawei’s and Cambricon’s domestic chips.

This coordinated national strategy signals a determined push for technological independence. The chip revolution is not just about faster processors. It’s about a fundamental reshaping of efficiency, supply chains, and the global balance of technological power.

Part Five: The Convergence — One Compounding Engine of Change

The mega-trends described above are not independent events. They are a “supersonic tsunami” precisely because they are converging and compounding each other. Each wave feeds the next, creating a series of powerful, self-reinforcing feedback loops that are accelerating the entire system at an exponential rate.

Feedback Loop 1: Efficient Chips and Abundant Energy. The insatiable energy demand of the AI infrastructure build-out created a massive economic incentive to solve two of technology’s grandest challenges: radically efficient computing and abundant clean power. The development of neuromorphic chips that offer up to 1,000x greater energy efficiency is a direct response to this pressure. As these chips move from labs to data centers, they will begin to bend the curve of AI’s energy consumption downwards. Simultaneously, the promise of nearly unlimited, carbon-free power from fusion and next-generation nuclear reactors removes the ultimate ceiling on AI’s growth. The prospect of gigawatt-scale data centers powered by dedicated fusion or SMR plants makes projects like OpenAI’s “Stargate” initiative — a planned $500 billion, 10GW AI supercomputer — not just feasible, but logical.

Feedback Loop 2: Massive Infrastructure and Model Capability. The unprecedented capital deployment by hyperscalers — nearly $700 billion in 2026 alone — is a direct, calculated response to the explosive revenue being generated by companies like Anthropic and OpenAI. They are building the “picks and shovels” for a gold rush that is already yielding enormous profits. This massive infrastructure then enables the next leap in AI capabilities. Access to vast clusters of GPUs is the primary ingredient for training more powerful and sophisticated models. The next generation of infrastructure currently being built will give rise to models with capabilities we can only begin to imagine. This is the engine of the AI revolution: revenue funds infrastructure, which creates capability, which generates more revenue.

Feedback Loop 3: Vertical Integration and Supply Chain Restructuring. The sheer scale of the infrastructure build-out and the critical importance of AI to companies like Tesla, Google, and Amazon have exposed the vulnerabilities of a globalized supply chain. This has triggered a powerful drive toward vertical integration. Tesla’s Terafab project is the most extreme example. This move, in turn, puts pressure on the rest of the industry — accelerating the trend of other tech giants designing their own custom chips to avoid being solely dependent on NVIDIA, while simultaneously solidifying the central role of TSMC as the indispensable manufacturer for all these competing designs.

Consider the full chain of causation: Anthropic’s 10x revenue growth justifies Amazon’s $200 billion in capital expenditure. That capital expenditure creates demand for NVIDIA GPUs, which in turn strains TSMC’s advanced packaging capacity, which accelerates Tesla’s push to build its own fab. The energy demand from all these new data centers revives Three Mile Island and funds Helion’s fusion plant. And the AI models trained in those data centers are then used by DeepMind to make fusion reactors work better, which will eventually provide the cheap, clean energy to power an even larger generation of data centers. Every link in the chain strengthens every other link.

Part Six: What It Means For You

The supersonic tsunami of converging technologies is not an abstract phenomenon for futurists to debate. It is a present-day reality that is actively reshaping the landscape for every individual and organization. Navigating this transformation requires a fundamental shift in mindset — from one of scarcity and incrementalism to one of abundance and exponential thinking.

If you’re an entrepreneur, design for abundance. Assume intelligence is becoming free. With tools like Claude Code and GitHub Copilot, a single developer can now have the productivity of a small team. Stop building businesses predicated on the high cost of cognitive labor. Instead, ask: what becomes possible when intelligence is a cheap, scalable utility? Assume energy is becoming unlimited. The convergence of fusion and next-generation nuclear power points to a future of abundant, clean energy. What energy-intensive processes become viable?

Think about large-scale manufacturing, vertical farming, water desalination, or direct air carbon capture. And assume labor is becoming robotic. With the rise of humanoid robots like Tesla’s Optimus, the cost of physical labor is set to fall dramatically. Your competitive advantage is no longer just better execution. It is the audacity of your imagination about what tomorrow’s abundance makes possible today.

If you’re an investor, own the infrastructure. In a gold rush, the most reliable way to build generational wealth is to sell the picks and shovels. The AI revolution is the biggest gold rush in history, and the “picks and shovels” are the foundational infrastructure being built to support it. The most durable investments will be in the companies that provide the non-negotiable inputs for the AI economy: AI chips, energy, data center infrastructure, and robotics platforms. But watch for the second-order plays.

The most obvious investments — NVIDIA, the hyperscalers — are already priced for dominance. The savvier opportunities may lie in the companies that supply the cooling systems for AI data centers, the firms developing the specialized electrical transformers needed for gigawatt-scale facilities, and the utilities positioned to benefit from the surge in power demand.

If you’re a CEO, prepare for the stress test. Your industry is about to be fundamentally stress-tested by the new economics of AI. Convene your leadership team and ask: what would our business look like if our competitors had access to free compute, unlimited energy, and scalable robotic labor? Stop thinking of AI as a software tool to be managed by the CIO.

Start thinking of it as a new form of capital that can be deployed by the COO to augment and automate work across the entire organization — in legal, marketing, finance, HR, and operations. Set a 90-day AI integration target. Identify the three highest-cost, most repetitive processes in your organization and mandate that your teams prototype an AI-augmented version within 90 days. The companies that are successfully integrating AI are treating it not as a one-time IT project, but as an ongoing operational discipline.

If you’re a student, collaborate, don’t compete. The biggest mistake your generation can make is to train for a job that can be automated by AI. Treat AI as your indispensable thinking partner. The new measure of productivity is not what you can do on your own, but what you can accomplish in partnership with an AI. Develop T-shaped expertise — deep knowledge in one domain combined with broad literacy across adjacent fields.

A biologist who understands machine learning, a lawyer who can write code, a designer who grasps data science — these hybrid profiles will be uniquely positioned to direct AI tools toward novel, high-value applications that neither a pure specialist nor a pure AI could conceive alone. And design your learning for a 100-year life. With breakthroughs in AI-accelerated longevity research, it’s increasingly plausible that you will have 100+ healthy, productive years. The old model of learning for your first job is obsolete.

Conclusion: The Wave Is Here

The evidence is overwhelming and the trajectory is clear. The “Supersonic Tsunami” is not a distant forecast. It is the defining reality of our time.

We have seen how the abstract promise of AI has ignited a financial explosion of unprecedented scale, with companies like Anthropic and OpenAI achieving revenue growth that defies all historical precedent. This is not a bubble. It is the economic validation of a technology that has crossed the threshold from tool to a new form of labor.

We have charted the physical manifestation of this boom: a multi-trillion-dollar infrastructure build-out led by the world’s largest corporations, who are constructing “AI factories” at a scale that is altering the global economic landscape and straining our industrial capacity to its limits.

We have examined the critical bottleneck of energy and the extraordinary solutions emerging to solve it. The race for commercial fusion power is accelerating, with private companies and public labs shattering records on a monthly basis, while a nuclear renaissance is providing the immediate, reliable power needed to fuel the AI revolution.

And we have explored the revolution at the heart of it all — in the silicon chips that form the substrate of this new world. Brain-inspired neuromorphic designs promise a future of radical efficiency, while the entire semiconductor industry is being restructured around the immense strategic value of custom AI hardware and the geopolitical race for technological sovereignty.

These are not separate stories. They are one story. The revenue from AI funds the infrastructure. The infrastructure’s energy demand accelerates the arrival of fusion. AI itself helps solve the physics of fusion. The scale of the build-out forces a restructuring of the chip industry. Each wave amplifies the next, creating a self-reinforcing cycle of exponential change.

The future where intelligence is a utility, energy is abundant, and labor is robotic is no longer a far-off vision. It is being built, funded, and deployed today. The implications are staggering, presenting both immense opportunity and existential risk for every individual, company, and nation. The choice is no longer whether to engage with this transformation, but how.

The people who see the convergence — who understand that compute, energy, intelligence, and supply chains are now part of a single, compounding system — are the ones who will build what comes next.

The tsunami is here. The only question that remains is: are you ready to ride it?